0DTE SPY vs SPX Options: 7 Differences for Choosing

Learn how the differences between SPX and SPY options can shape your 0DTE trading approach.

SPX (S&P 500 Index) and SPY (SPDR S&P 500 ETF) options are among the most liquid in the market. Their prices move together, but differences in settlement, contract size, expiration, taxes, and costs can impact your strategy.

In this article, we'll cover seven key distinctions to help 0DTE option traders choose.

Highlights

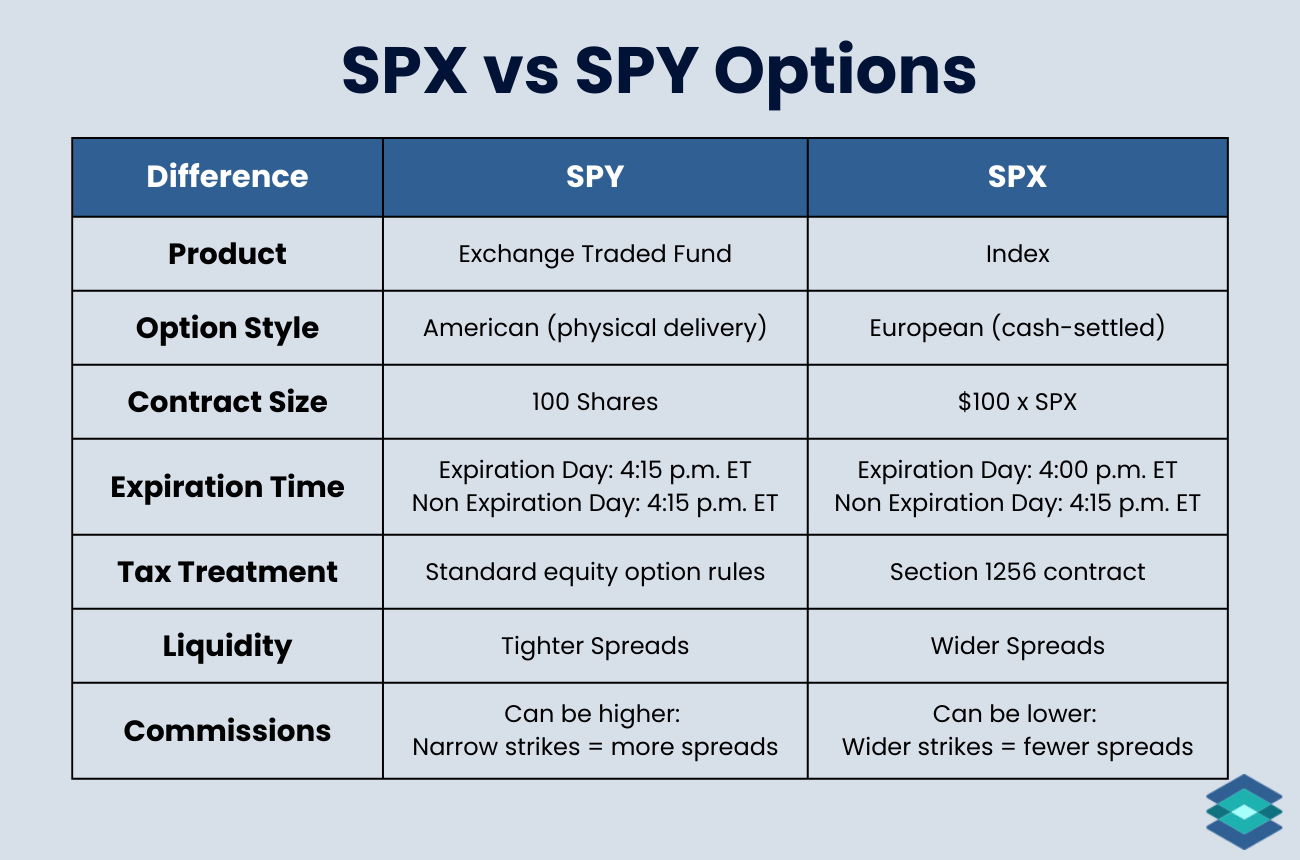

- Product Type: SPY is an ETF with physical share delivery on assignment; SPX is an index with cash settlement, eliminating share delivery risk.

- Contract Size: SPY controls 100 shares of the ETF; SPX uses a $100 multiplier on the index, making one contract about 10x larger in notional value.

- Expiration Time: On non-expiration days, both trade until 4:15 p.m. ET. On expiration day (0DTE), SPY still trades until 4:15 p.m. ET, while SPX PM-settled options trade until 4 p.m. ET.

- Tax Treatment: SPX qualifies for Section 1256 60/40 tax treatment (usually preferred by traders); SPY follows standard equity option tax rules based on holding period.

- Liquidity & Costs: SPY has tighter spreads and more strikes but potentially higher commissions due to smaller contract sizes; SPX has wider spreads but fewer contracts needed.

Without further ado, let's start with the 7 major differences between SPY and SPX options.

1. ETFs (SPY) vs Indices (SPX)

Exchange-traded funds (ETFs) like SPY have tradable underlying assets. You can buy or sell them just like a stock, and each share represents a portion of the ETF’s holdings.

Indices like SPX are benchmarks. They do not have tradable shares. Instead, you can trade products linked to it, like futures contracts or options.

SPY is designed to mirror the price and performance of the S&P 500 Index (SPX) by holding the same 500 stocks, each weighted according to the index’s methodology. Buying the 500 individual stocks yourself would be expensive, time-consuming, and a rebalancing headache. SPY does that work for you, for a small management fee.

Here are a few different indices and popular ETFs that aim to mirror their performance.

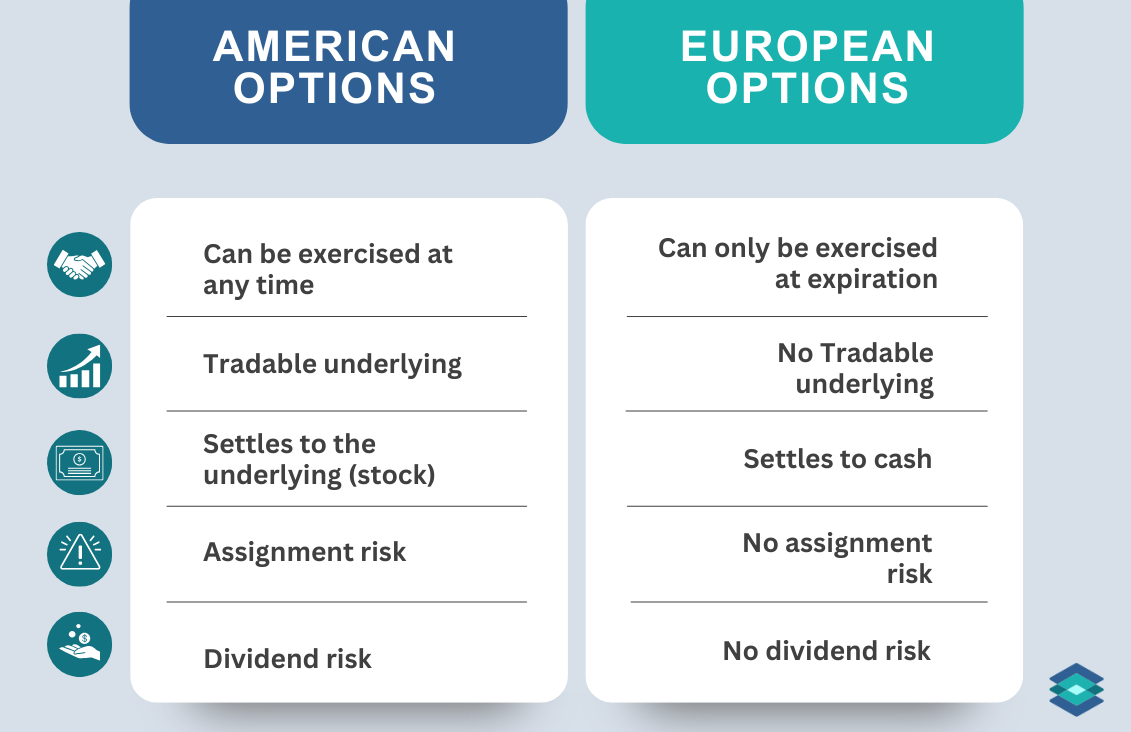

2. American vs European Style Options

In the US, most stock and ETF options are American-style. This means that when an option is assigned or exercised, the underlying shares change hands. If you are short a call and it expires in the money, you will deliver 100 long shares to the owner of the call at the strike price, leaving you short 100 shares. This is called physical delivery.

European-style options, like SPX index options, do not have an underlying asset to deliver. Instead, they are settled through a simple transfer of cash between accounts: a debit to the losing side and a credit to the winning side. This is why they are called cash-settled.

Take a look at the table below to see how this works. ABC is an ETF and XYZ is an index. In both examples, you are short a call option that expires in the money and therefore is assigned:

3. Contract Size Differences

There are significant differences in the contract sizes of SPY and SPX options:

- SPY options represent 100 shares of the ETF. If SPY is trading at $500, one contract controls $50,000 of notional value.

- SPX options use a $100 multiplier on the index price. If SPX is trading at 5,000, one SPX contract controls $500,000 of notional value, ten times larger than SPY.

This size difference makes SPX popular with institutional traders seeking large exposure, while SPY offers more flexible sizing for smaller accounts.

4. Expiration Time

Both SPX and SPY options trade until 4:15 p.m. on non-expiration days. There are some subtle yet important differences in when SPY and SPX stop trading on expiration day, as seen below:

I can tell you firsthand you don't want to be stuck trading out of large ETF options positions near the bell. The liquidity can be horrendous.

SPX also offers AM-settled options (SPXAM), which stop trading at 4:00 p.m. ET the day before expiration and settle the next morning based on the opening prices of the S&P 500 stocks.

5. Tax Treatment

Index options can offer tax advantages for some traders because of how they are classified:

- SPX (Index options) - Section 1256 contracts with a 60% long-term / 40% short-term capital gains split, regardless of holding period. Marked to market at year-end, which can simplify reporting.

- SPY (ETF options) - Standard equity option tax rules, where gains are short-term or long-term based on the actual holding period. No 60/40 split and no year-end mark-to-market.

For example, if you had a $1,000 profit on a ten day SPY put trade, the entire amount would be taxed as short-term capital gains because you held the position for one year or less.

If you had the same $1,000 profit on SPX, $600 would be taxed at the long-term capital gains rate and $400 at the short-term rate, regardless of how long the trade was held. Short-term rates are generally higher, so this split can reduce the overall tax bill for active traders.

Of course, all tax situations are different, so make sure to ask your tax professional which is right for you.

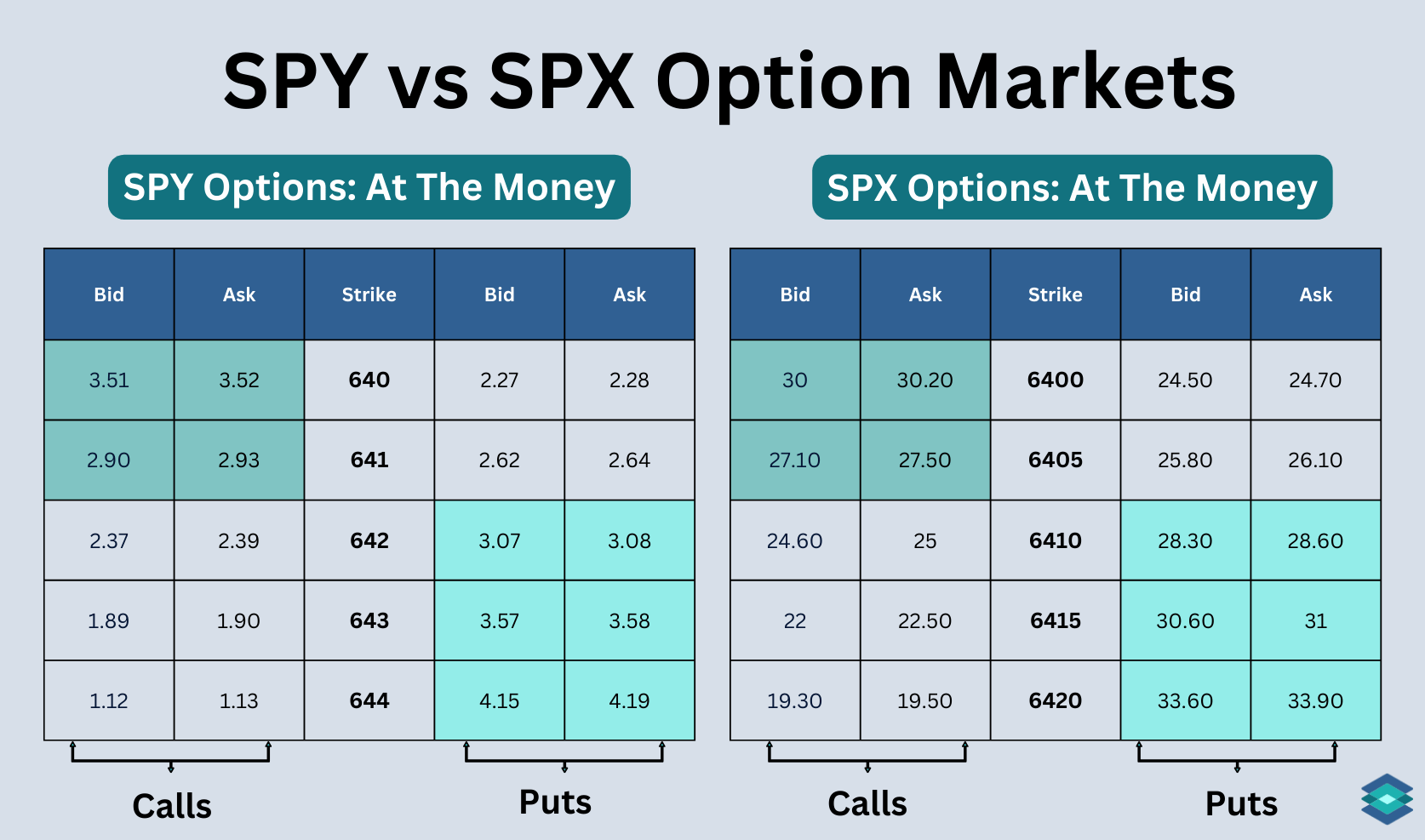

6. Liquidity

Both SPY and SPX options are highly liquid, but there are differences:

- SPY: Very tight bid-ask spreads, usually $0.01 for active strike prices.

- SPX: More institutional flow with deep size but generally wider markets.

We can see how SPX comparatively has wider markets than SPY for the below options chains showing calls and puts:

Always start at the midpoint when trading any options, particularly in wider markets like SPX. If you do not get filled, work the order up or down in penny or nickel increments.

📖 Read more about options liquidity metrics, like open interest and volume here!

7. Commissions

SPY traders often pay more in commissions than SPX traders. This is because SPY lists strikes at every $1 and sometimes $0.50, making it possible to build $1-wide or even $0.50-wide spreads. While this offers greater precision, it also means trading more contracts, which can drive up commission costs.

SPX options only offer $5-wide strikes, so similar positions require fewer contracts. The wider intervals reduce precision and increase risk, but can lower overall commissions compared to trading narrow SPY spreads.

Index options can directly cost traders more commission as well. This is because index options have higher OCC and Cboe exchange fees, and brokers sometimes pass these costs on to customers.

Final Word

SPX and SPY options may track the same market, but the way they trade, settle, and are taxed can lead to very different outcomes. SPY’s smaller contract size, tighter spreads, and physical settlement make it approachable for more traders, while SPX’s larger notional value, cash settlement, and tax advantages appeal to those seeking efficiency and scale.

The right choice depends on your account size, risk tolerance, and strategy. By understanding these key differences, you can choose the product that aligns best with your trading goals.

⚠️ Trading SPX and SPY options involves substantial risk and is not suitable for all investors. Examples in this article are for educational purposes only and do not include commissions or fees, which can significantly affect trade outcomes. Always review The Characteristics and Risks of Standardized Options before trading and ensure you understand how each product works before committing capital.

FAQ

It depends on your goals. SPY offers smaller position sizes, tighter spreads, and more strikes, while SPX gives you larger contract value, cash settlement, and favorable tax treatment.

SPX is the S&P 500 index, while SPY is an ETF priced at roughly one tenth of the index so it is more accessible to traders.

SPX’s main appeal is cash settlement, the 60/40 tax split, and fewer contracts needed for large notional exposure. It is popular with institutions and high-volume traders.

Yes. SPX options are widely traded, available in multiple expirations including 0DTE, and come in both AM-settled and PM-settled versions.

Wider bid ask spreads and larger contract size can make SPX less flexible for smaller accounts, and position sizing is less precise compared to SPY.

They are Section 1256 contracts, which means profits are taxed 60 percent at the long-term rate and 40 percent at the short-term rate regardless of how long you held the trade.

0DTE options are options that expire the same day they’re traded. They are generally high risk, high reward trades.

No. Options only trade during regular market hours. After the close, you can’t make any changes, so you need to manage your trades before the bell.

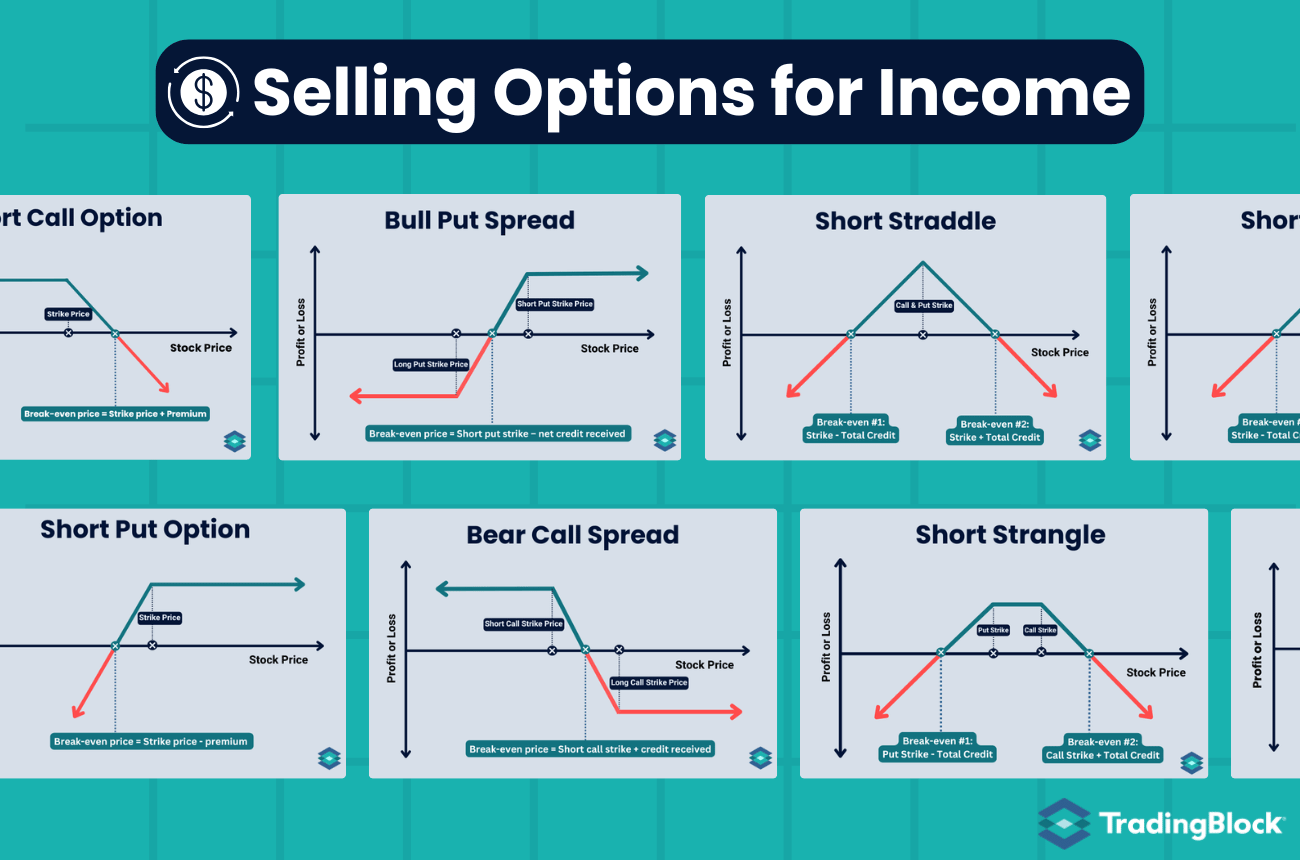

The best 0DTE options strategy depends on your market outlook. If you expect a big move, net debit strategies like long calls or puts may work. If you expect the market to stay put, selling premium can make take advantage of time decay. Think short puts, short iron condors, or short straddles.

.png)

.png)

.png)