Option Theta Explained: Time Decay for Beginners

In options trading, time decay refers to the erosion of an option's value as its expiration date approaches. The option Greek theta quantifies this decay, showing how much value an option loses daily, assuming other factors (like implied volatility and the underlying price) remain constant.

In options trading, time decay (theta) measures how much value an option loses each day as expiration approaches. Theta is always negative for long options, meaning buyers lose value over time while sellers benefit from this time decay.

For example, if an option has a theta of -0.05, its price will drop by $0.05 daily, assuming other factors remain constant. Time decay accelerates as expiration nears, making it a key consideration for buyers and sellers in options trading.

Highlights

- Theta is always negative for long options – It represents the daily loss in an option’s value due to time decay.

- Time decay accelerates as expiration nears – Options lose extrinsic value faster in the final weeks and days before expiration.

- At-the-money (ATM) options have the highest theta – These options hold the most extrinsic value, making them more sensitive to time decay.

- Option sellers benefit from theta – Strategies like short calls and short puts, credit spreads, short iron condors, and short straddles profit from time decay.

What is Time Decay?

Time decay is the gradual erosion of an option’s value as expiration approaches. Unlike stocks, option contracts have an expiration date. For a long option contract to be profitable, the option must be in-the-money (ITM) by expiration. You also need to account for the premium paid to calculate breakeven levels.

- Call option breakeven = Strike price + Premium paid

- Put option breakeven = Strike price - Premium paid

An option is only profitable if it’s in-the-money (ITM) at expiration. As time passes, an out-of-the-money (OTM) option faces increasing pressure from time decay, making it less likely to become profitable. The closer it gets to expiration, the faster its value erodes—eventually reaching zero if it stays OTM on expiration.

Time Decay vs Price

Most beginner option traders learn the hard way that a stock moving in the right direction isn’t always enough to make an option gain value.

For example, let’s say you own a 100 strike price call option on ABC, trading at $95 per share, and your option expires in three days.

Even if ABC is up on a given day, it may not be up enough to make your option profitable. How much is it up? That’s the key.

The image below shows how the value of a long call option slowly (then quickly) deteriorates as the underlying asset's value stagnates in price.

Options trading is all about the magnitude of the move (and implied volatility). If the move isn’t big enough, time decay eats away at your option’s extrinsic value, making it harder to profit—even when you're technically “right” about the direction.

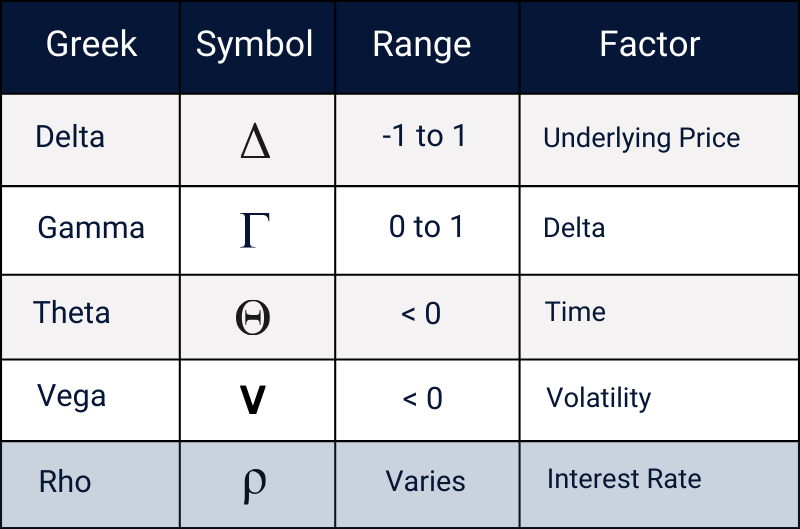

Intro to The Greeks

The Greeks are a set of risk metrics that measure an option’s sensitivity to different factors. The most important thing to know about the Greeks is that they are forward-looking—they don’t tell you what has happened but what may happen under different scenarios.

For example, the Greek delta measures how an option may react to a $1 move up or down in the underlying stock, ETF, or other asset. Each Greek provides insight into how an option's price could change based on movement, time, or volatility (vega).

📖 What is the Greek Gamma and How Does it Work?

What is Theta?

Theta is the option Greek related to time. It tells us how much value an option will shed with the passage of precisely one day. To be sure, theta makes a lot of assumptions about the future, including:

- The price of the underlying asset stays the same

- Implied volatility stays the same

Markets are in a state of constant flux, so it’s important to remember that theta is not a fixed rule—it’s an estimate. Its value is also constantly changing to align with shifts in market conditions.

How Does Theta Work?

Theta is not linear. Time decay accelerates as expiration approaches. This is because options lose extrinsic value faster when there’s less time for the underlying to move.

This means that if you're buying options, your best bet is to avoid holding positions in the red zone, where time decay is most aggressive. On the other hand, if you're selling options, this decline in value works in your favor, benefiting all short options.

Theta also has a direct relationship with the moneyness of an option. More on that to come.

Theta Trade Example

Let’s now take a look at a trade example to see how theta affects the value of an ABC call option over time. This example assumes the underlying asset's price (ABC) does not change in value.

Initial Trade Setup:

- Stock Price: $100 (constant)

- Option Type: At-the-month (ATM) Call

- Strike Price: $100

- Days to Expiration: 60 days

- Initial Option Price: $7.00

- Theta at Start: -$0.06 per day

And here’s how this looks on a chart. Remember that we assume the underlying stock price and implied volatility stay the same here.

Here’s what we can draw from the above trade example:

Key Takeaways

- Theta Decay Starts Slow (60-45 Days):

- A gradual decline in option value, but still retains time premium.

- Accelerates in Last 45 Days:

- As expiration nears, theta decay increases significantly.

- Final 10 Days Are Brutal for Option Buyers:

- Most extrinsic value is wiped out rapidly.

- Great for Option Sellers:

- Traders selling options (like covered calls or puts) benefit from this accelerated decay.

Theta and Moneyness

Theta also varies based on an option’s extrinsic value, which depends on its moneyness. The more extrinsic value an option has, the greater its theta decay.

- ATM options have the highest theta – Since they contain the most extrinsic value, they experience the fastest time decay.

- OTM and ITM options have lower theta – These options have less extrinsic value, so their decay rate is slower.

- Theta decay accelerates in the final weeks – The closer an option is to expiration, the more rapidly its extrinsic value erodes, particularly for ATM options.

Understanding how moneyness affects theta is a great starting point for determining when to enter and exit trades.

Why is Theta Always Negative?

Unlike some other Greeks, theta's value is always negative for long options. This is because options lose extrinsic value as time passes, meaning the option premium naturally declines over time.

We can see this below on the options chain from the TradingBlock platform:

What does this mean for you as a trader?

- For option buyers, theta is a downside—each day that passes reduces the option’s value, all else equal.

- For option sellers, theta is beneficial—it allows them to profit as time decay erodes the price of short options.

Since time only moves forward (at least for now), theta decay is inevitable. It works against long options while benefiting short positions.

So, why would anyone buy a call or put option? Traders are drawn to options for the leverage they offer. Long options can generate substantial returns if you expect a significant and rapid move in the underlying asset. However, this is the exception rather than the rule.

“Positive” vs Negative Theta

So we just learned that all theta is negative, which may have you scratching your head at this comparison. However, traders use the terms positive and negative theta to describe whether time decay works for or against their positions. When you are short options, you are actually short theta.

- When an option position benefits from the passage of time, it is said to be positive theta. This would have to be a net short position, whether in calls, puts or a combination of both.

- When an option position loses value over time, it has negative theta. This relates to long options, where time decay works against the trader, requiring the underlying asset to move enough to offset theta decay before expiration.

Theta and Extrinsic Value

The price of all options is made up of two components:

- Intrinsic value – The built-in value of an option, or how far it is in the money.

- Extrinsic value – The portion of the premium that isn’t intrinsic value, mostly driven by time and implied volatility (IV).

Extrinsic value is where theta comes into play—as time passes, this portion of an option’s price naturally decays. Intrinsic value does not incorporate time—it’s directly tied to the underlying asset’s price. If an option is in the money, it has intrinsic value. The deeper it is in the money, the more intrinsic value it holds.

You can see this in the blue area on the chart below. Notice how, unlike extrinsic value, this value is tethered directly to the price of the underlying asset.

.png)

Notice how the option’s extrinsic value (time value) steadily declines as the options expiration approaches—even as the stock price rises. If the move isn’t big or fast enough, time decay still eats away at the option’s value. That’s the detrimental effect of time decay.

Option Theta Calculator & Visualizer

Want to see how theta affects options over time? Try it out for yourself—interact with our Theta Calculator below!

🧮 Click Here to See All of Our Option Calculators!

Theta: Option Strategies

Let's now explore some different options trading strategies associated with positive and negative theta.

Theta and LEAP Options

Everything we've covered shows that options lose value faster as expiration nears, with time decay ramping up around the 45-day mark.

So, what about LEAPS? Are they the best way to speculate on long-term price moves since they theoretically have the least exposure to time decay?

As we can see, theta has the least impact on LEAPS, making these options a solid choice for long-term bullish or bearish positions. With more time until expiration, they hold their extrinsic value longer, reducing the impact of time decay compared to shorter-term options.

However, keep in mind that LEAPS typically come with high premiums. While time decay affects them less, LEAP buyers take on significantly more premium risk.

Theta and 0DTE Options

If you’re purchasing 0DTE (zero days to expiration) options, you’re taking a high-risk, high-reward position that the underlying asset is about to make a big move quickly. These options have little time remaining, so you depend on price action and volatility. Theta decay will decimate your position if the stock doesn’t move quickly enough or in the right direction, sometimes in a matter of minutes.

If you’re selling 0DTE options, you’re on the other side of that equation, looking to capture premium through fast time decay. With little or no extrinsic value remaining, you’re profiting from the quickly approaching expiration. But here’s the catch: your gamma risk is very high. One sharp move against your position and the losses can add up quickly.

Theta and 0DTE Example

Let's jump over to the TradingBlock platform and compare two SPY (SPDR S&P 500 ETF Trust) expiration cycles: one expiring today and another expiring in 71 days.

Here are a few comparisons to note for the above two option expirations:

⚠️ Be mindful of commissions and fees not included in our examples. Always understand the risks associated with investing and review The Characteristics and Risks of Standardized Options before trading options.

FAQ

When theta is high, the time decay of options is accelerating, which means that options lose value more quickly as expiration approaches.

Negative theta is not good for option buyers as it implies the option's value decreases as time passes. All theta is negative for long options.

At-the-money (ATM) options have the highest theta because they have the greatest time value, so time decay affects them most.

Yes, theta measures the time decay for an option contract over one day, though it is in a state of constant flux with the market.

A few great options strategies to capitalize from time decay include selling covered calls, puts, iron condors, and vertical spreads (calls or puts).

0DTE (zero days to expiration) options decay quickly due to their high time sensitivity.

.png)

.png)