Option Premiums: Definition, Formulas & Charts

In options trading, the "premium" refers to the price of an options contract, which includes both intrinsic and extrinsic value.

.png)

In options trading, buyers pay the premium, while sellers receive it. This article will explore the components of option premiums, how they are calculated, and why they fluctuate over time.

Highlights

- The "premium" in options trading is the price of an options contract, which includes both intrinsic and extrinsic value.

- Buyers pay the premium (debit), while sellers receive it (credit).

- Intrinsic value reflects the amount an option is in-the-money, based simply on the difference between the strike price and underlying asset price (moneyness).

- Extrinsic value represents all value that is not intrinsic (time and volatility), and decreases as expiration approaches.

What Is an Option Premium?

In options trading, the ‘premium’ refers to the price of an options contract. When you purchase an option (go long) the premium paid is referred to as the ‘debit’ paid. When you sell an option (go short) the premium received is referred to as the ‘credit’ received.

Option premiums fluctuate constantly with the underlying asset, whether that be a stock, index, ETF, or commodity. Factors beyond price that influence option premium include days until expiration (DTE) and volatility.

Before we discuss option premiums in more detail, it will help to have a basic understanding of how options are priced.

Intro to Option Pricing

There are three methods that market makers use to price the premiums of options contracts:

- Black-Scholes Model

- Binomial Model

- Monte Carlo Simulation

Black-Scholes is used primarily to price European-style options, which include most index options.

The Binomial Model is used to price America-style options, as this model incorporates the possibility of early exercise and assignment in most stock and ETF options—something that does not typically happen in European-style options.

Both models approach the ‘extrinsic’ value of an option differently, as intrinsic value is straightforward. We will explore both of these option premium components in detail below. But first, it will help to understand the relationship between 'moneyness' and option premium.

Option Premiums and Moneyness

Option premiums have a direct relationship with the moneyness of an options contract. In-the-money (ITM) options will have a higher premium than out-of-the-money options (OTM). This is because ITM options are closer to the underlying asset's market price, meaning they have a higher percent chance of expiring ITM.

Take a look at the below image of SPY (SPDR S&P 500 ETF Trust) call options on the TradingBlock platform. Notice how the premium of these options diminishes as the strike price drifts further away from the price of the ETF.

.png)

This should make sense - if the stock is trading at ~$598/share, doesn’t the 598 call option have a higher likelihood of closing ITM on expiration than the 600 call option? Of course. Remember, if an option closes OTM on expiration, it will have zero value.

💧 Options Trading: Liquidity Essentials

How Do You Calculate an Option Premium?

The price of any call or put option consists of summing together two components: intrinsic and extrinsic value.

- Intrinsic Value: The value an option has if it were to be exercised immediately

- Extrinsic value: All other option value, such as time left until expiration and volatility.

An option can have all extrinsic value, all intrinsic value, or a combination of each.

Next, we will take a closer look at each of these components.

Option Premium: Intrinsic Value Factors

Determining an option's intrinsic value is easy; it is simply the amount by which the option is in-the-money (ITM).

For example, if a stock trades at $100/share, all call options at or above this price will have $0 of intrinsic value since they are all out-of-the-money (OTM)

But does this mean that these OTM options have no value? Of course not.

These options have 30 days until expiration (DTE). Isn’t there a chance ABC could rally to $102 during this time? This time element of an option is referred to as extrinsic value, which we will learn next.

⚠️ Besides the initial debit paid or margin, it is essential to consider the commissions and fees associated with most options transactions when calculating net profit or loss. These fees can significantly impact the overall return on investment and should be factored into all trades placed.

Option Premium: Extrinsic Value Factors

If intrinsic value represents the exercise value of an option at any given time, extrinsic value represents any and all value above intrinsic value.

This extra value reflects the potential for the option to become profitable before expiration, and it considers many factors.

- Time until expiration

- Implied volatility

- Dividends

- Interest rate

Let’s now explore these one by one:

1. Time Until Expiration

The longer the time to expiration, the higher the extrinsic value of an option. This is because time increases the likelihood that the option's price could move favorably.

Below are two SPY (SPDR S&P 500 ETF Trust) put option chains with different expirations: the top options expire today, and the lower options expire in 7 days.

.png)

The options expiring today still have about four hours of trading left. If we were to look at these option premiums just a few seconds before the close, the vast majority of the OTM options would have a zero bid. This is because there is no time left, and their value is composed entirely of intrinsic value or no value at all.

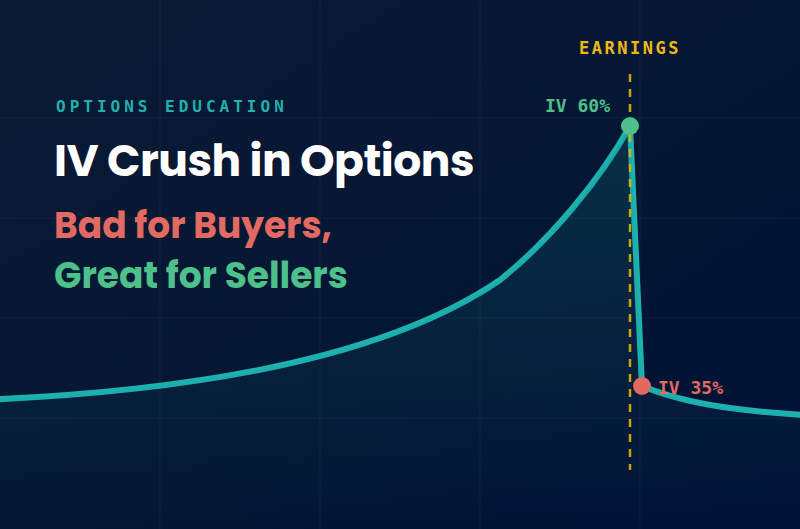

This introduces us to something called time decay, which is represented by the option Greek theta.

To see time decay, or "theta," in action, examine the visual below, showing only an option's extrinsic value over time. You'll notice that this value declines exponentially as expiration nears.

2. Implied Volatility

In addition to time, implied volatility also plays a significant role in determining the extrinsic value of call and put options.

For example, let's take two different underlying ETFs:

- SPY (SPDR S&P 500 ETF Trust)

- SPXL (Direxion Daily S&P 500 Bull 3X Shares)

SPXL is a leveraged ETF that aims to provide 3x exposure to the S&P 500 index. Therefore, wouldn’t you expect the options on SPXL to trade at a relative premium to SPY, which tracks the same index on a 1x1 basis?

Notice below how the implied volatility (IV) is three times greater in the SPXL options than in SPY, which leads to a relative increase in extrinsic value.

3. Dividends

Owning equities comes with rights, like receiving dividends (if the company issues them), but options don’t carry these rights. As a dividend date approaches, extrinsic value in options is decreased, particularly for in-the-money calls. Many owners of in-the-money call options will exercise early before the ex-dividend date to receive the dividend by owning the stock.

If you’re short an in-the-money call option before the ex-dividend date, it’s wise to exit the position to avoid the risk of being assigned, as the call holder may choose to exercise to capture the dividend.

4. Interest Rates

Interest rates also influence the extrinsic value of an option, though to a lesser degree than the factors mentioned above. This effect is more pronounced in long-dated options, or LEAPS options, which expire in over a year. When holding an option for more than a year, consider the potential return you could have earned if you had invested that money at the risk-free rate. This “opportunity cost” is factored into the extrinsic portion of the option premium.

Option Premium Example

Now that we’ve covered both intrinsic and extrinsic value, let’s look at an example. Here are two key takeaways:

- Intrinsic value is simply the relationship between the strike price and the underlying price, without considering time.

- Extrinsic value decreases as time passes.

Explore Options Trading With Virtual Trading

With TradingBlock’s Virtual Trading platform, you can trade options in a simulated environment. Check it out below today!

FAQ

The cost of an option premium takes into consideration an option's intrinsic and extrinsic value. Together, these two components compose the total value of any options contract.

Options premiums tend to be high when the underlying asset is very volatile and when expiration is far off.

The strike price is the price at which the owner of an option can receive the underlying assets. The option premium is the cost to acquire an option.

No, you cannot directly withdraw the premium of an option. However, if you are the option seller, you receive a credit for the option value when you sell it. If the option you sold expires out of the money, you keep the entire premium and can then withdraw those funds from your account.

In options trading, the buyer pays a debit equal to the amount of the option premium to acquire the option. When you sell an option, the seller receives the option premium as a credit. The premium of an option fluctuates with the value of the underlying assets.

If you’re long an option, you’re at risk of a max loss if the option is valued at zero, meaning you lose the entire premium paid. On the other hand, if you’re the option seller and the option’s value drops to zero, you have collected all the credit received at a profit.

However, options aren’t fully settled until expiration, so it’s often smart to close out short positions as expiration nears. This may not be possible for long options if they are zero bid.

Options settle in one business day (T+1). If an option is in-the-money and exercised, the stock (or cash, for index options) will appear in your trading account the next business day.

When you sell an option, you receive the premium as a credit to your account as soon as the trade is executed.

.png)