Option Delta Explained: The Greeks for Beginners

The delta of an options contract tells us how much the price of an option is expected to change relative to a $1 move in the price of the underlying asset.

.png)

If you're a serious options trader, you must understand how delta works. In this article, we'll explain how this key option Greek reveals your directional risk and discuss strategies to effectively manage it.

Highlights

- The delta of an option indicates how much its price is expected to change for every $1 move (up or down) in the underlying asset.

- Calls have a positive delta ranging from 0 to 1, while puts have a negative delta ranging from -1 to 0.

- Delta also tells us how many shares of stock an option behaves like and the probability of the option expiring in-the-money (ITM).

- Delta hedging involves buying or selling the underlying asset to create a delta-neutral position, which reduces directional risk.

What is Delta?

In options trading, delta indicates how much an option's price changes in response to a change in the underlying asset's price.

Delta is one of many Greeks in options trading, which are all forward-looking risk measures. They are like time travelers peering into the future and reporting back to us what may happen given a change in ‘X.’ For example, the option Greek vega forecasts how the price of an option might change if the volatility of the underlying asset increases or decreases.

Delta is straightforward as it pertains to changes in the underlying price. It tells us the expected move of a long call or put option for every $1 move (up or down) in the price of the stock or whatever underlying asset you’re trading. It’s always based on a $1 move, no matter the underlying price.

Delta and Market Direction

If you’re "long delta," you have a bullish expectation on the market. The more deltas you own, the more bullish your position, as your portfolio will gain in value if the underlying asset's price rises.

The opposite is true for puts. If you have a short delta position, it reflects a bearish outlook, meaning you will profit from a decrease in the underlying asset’s price

If you’re market neutral, on the other hand, you will have a delta close to zero.

What’s great about delta is that it applies no matter how simple or complex your position is. Whether you have a single long call or a more complicated strategy like an iron condor, the net delta of your position gives you a clear understanding of your net directional risk.

What Does Delta Tell Us?

If you're only going to master one Greek, delta is the one to know. Delta is incredibly useful. I never place a trade before first checking the deltas.

Beyond showing how sensitive an option's price is to the underlying asset, delta also tells us:

- Probability of Expiring In-the-Money (ITM): Delta can also indicate the odds of an option expiring ITM. For instance, a 0.20 delta on an OTM call option means it has about a 20% chance of expiring ITM.

- Stock Equivalence: Delta tells you how many shares of stock your option “trades like”. For example, a call option with a delta of +0.35 would mimic owning 35 shares. A put option with a delta of -0.35 would mimic being short 35 shares.

The visual below, from the TradingBlock platform, shows the delta of call options on SPY (SPDR S&P 500 ETF Trust) expiring in 7 days.

See why Delta is so important now? Not incorporating delta into your trading strategy is like betting on a horse without knowing the odds.

🧮 Check out our Option Greeks Calculator here!

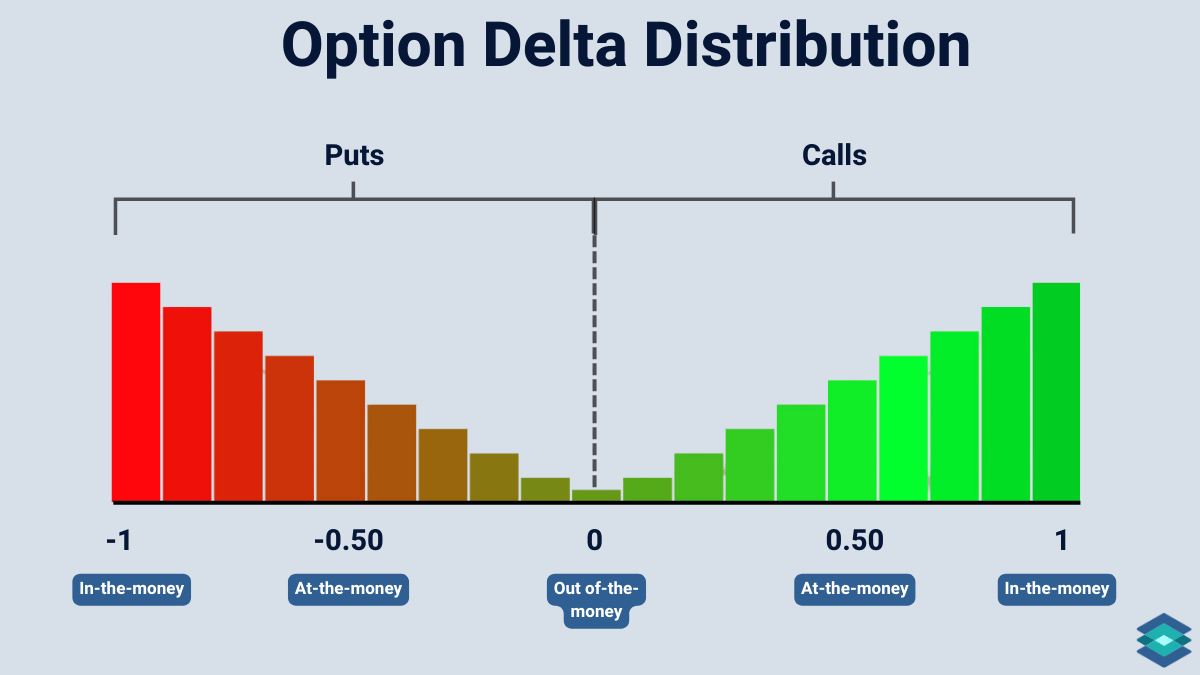

The Range of Delta

The delta of any options contract fluctuates but always stays between +1 and -1. Whether your delta is positive or negative depends on the type of option.

Call options have a positive delta, while put options have a negative delta due to their inverse relationship with the price of the underlying asset.

Call Options

- Delta ranges from 0 to +1.

- Far out-of-the-money calls have a delta near 0.

- Deep in-the-money calls have a delta near +1.

Put Options

- Delta ranges from 0 to -1.

- Far out-of-the-money puts have a delta near 0.

- Deep in-the-money puts have a delta near -1.

As we learned earlier, delta also tells us how many shares of stock an option trades like. Deep-in-the-money options have a delta of ±1, which means they trade like 100 shares of stock. Since these options closely mirror the stock price, many holders choose to exercise them to capture the intrinsic value. Because they trade almost like the stock itself, there’s little reason to keep holding the option, so long options are exercised to capture the intrinsic value.

Delta: Basic Example

Let’s say you own a 100-strike price call option on ABC, currently valued at $3.20. ABC’s stock price is at $100/share, meaning your option is at-the-money, and its delta is 0.50.

The stock price suddenly jumps from $100 to $101; here’s how this impacts your long call:

- Stock Price: $100 → $101

- Original Delta: +0.50

- Call Option Price: $3.20 → $3.70

- New Delta: +0.50 → +0.55

Since your option is now in-the-money, its delta has increased to 0.55. This means that for the next $1 rise in the stock price, the option’s value will increase by 55 cents.

📖 Understanding Liquidity in Options Trading

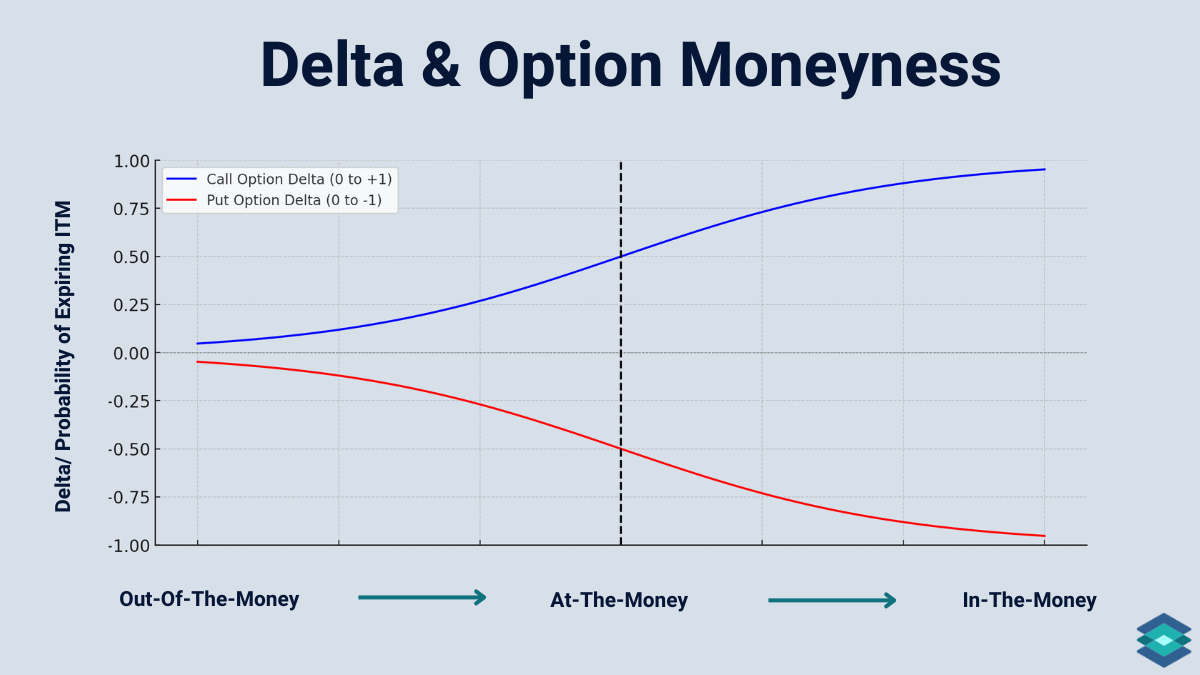

Option Moneyness & Deltas

An option's moneyness state will help determine its delta, if any. Some far out-of-the-money options have a zero delta.

You’ll notice that at-the-money (ATM) options for both calls and puts have a delta of 0.50 and -0.50, respectively. This means that these options have a 50% chance of expiring ITM. This should make sense as there is an equal probability that the underlying asset will finish above or below its current market price.

Delta & Time to Expiration

Delta is not static across option expirations. The further away the expiration, the flatter the delta curve becomes. This is shown in the below visual, which was constructed using delta values for various expirations from a real-world call options chain, which we will refer to as ABC.

Notice how the deltas converge toward +0.50 as the option approaches at-the-money. At this point, the probability of the option expiring in-the-money is approximately 50%, reflecting an equal likelihood of the underlying stock price moving above or below the strike price.

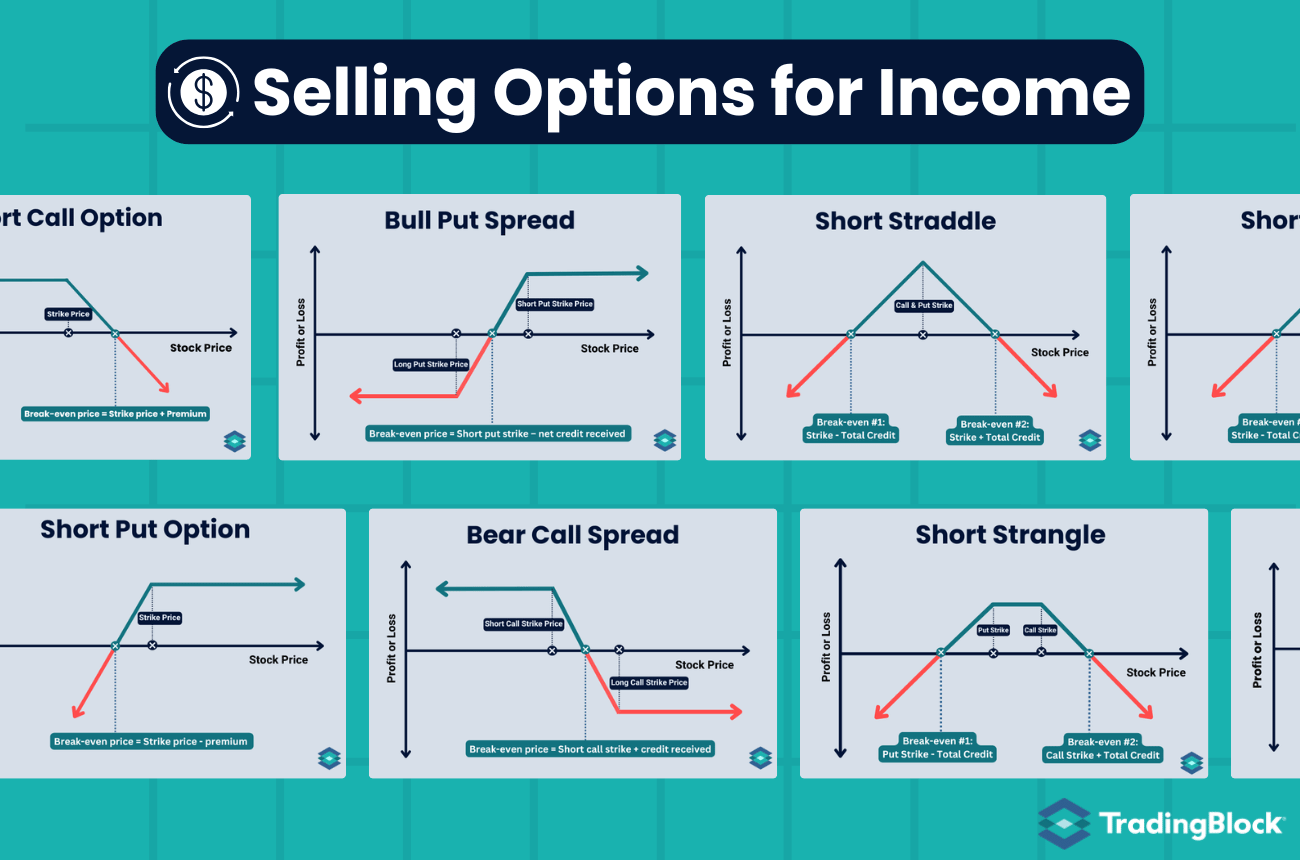

Delta and Option Strategies

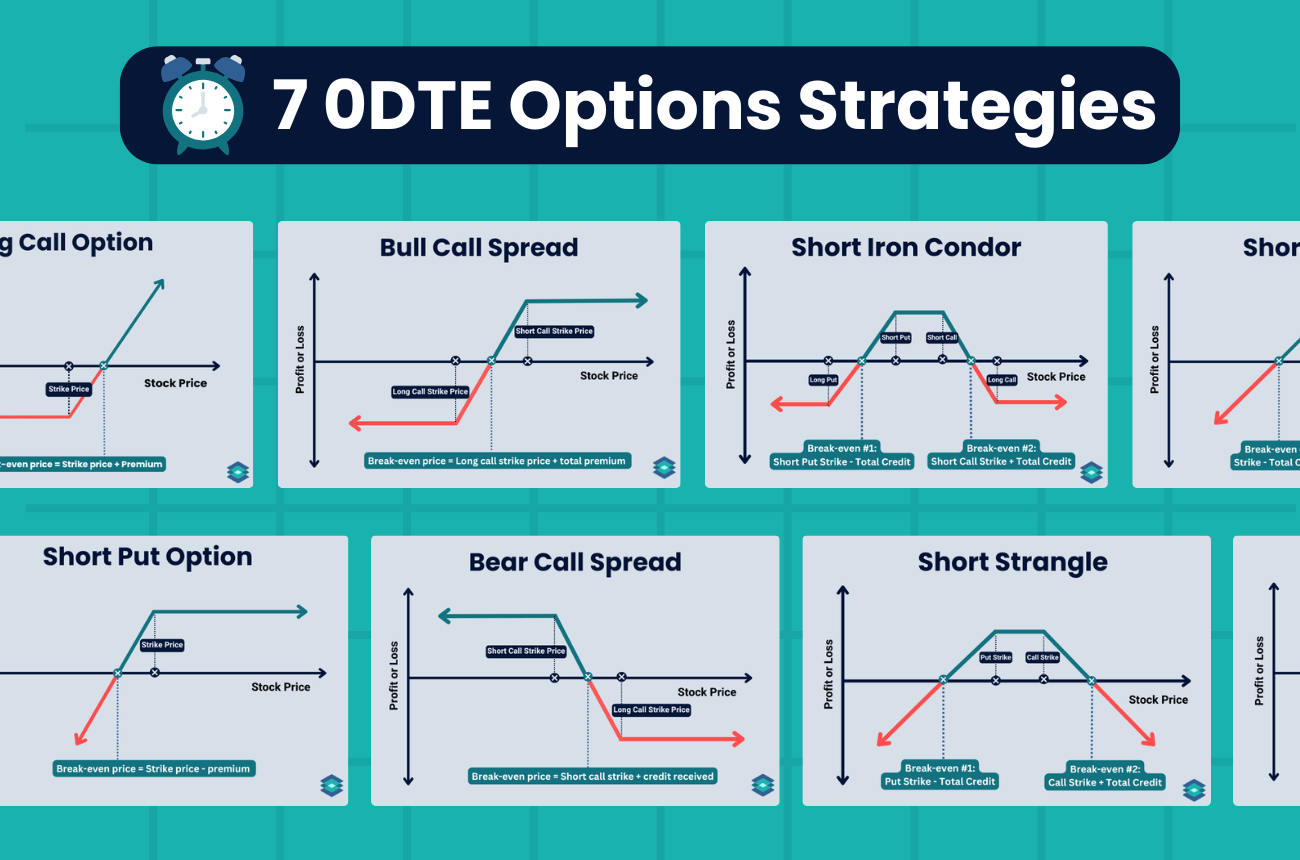

Delta is a great way to determine how bullish, bearish, or market-neutral any particular options trading strategy is. Here is a cheat sheet to help you get started with some basic strategies and their relationship to delta.

Intro to Delta Hedging

When I worked on a trade desk, I’d often talk to traders who had dozens of positions in a single underlying, usually SPX (S&P 500 Index). Managing all those long and short calls and puts would’ve been nearly impossible without delta. Why? Because a trader would have no clue how their net position reacts to changes in the underlying price!

Delta makes understanding a position's directional risk simple. It tells you your directional risk in a clean, straightforward way. Even if you had 500 option positions scattered across different expirations and strikes on a given stock, delta is all you need to know how bullish or bearish you are at any moment in time.

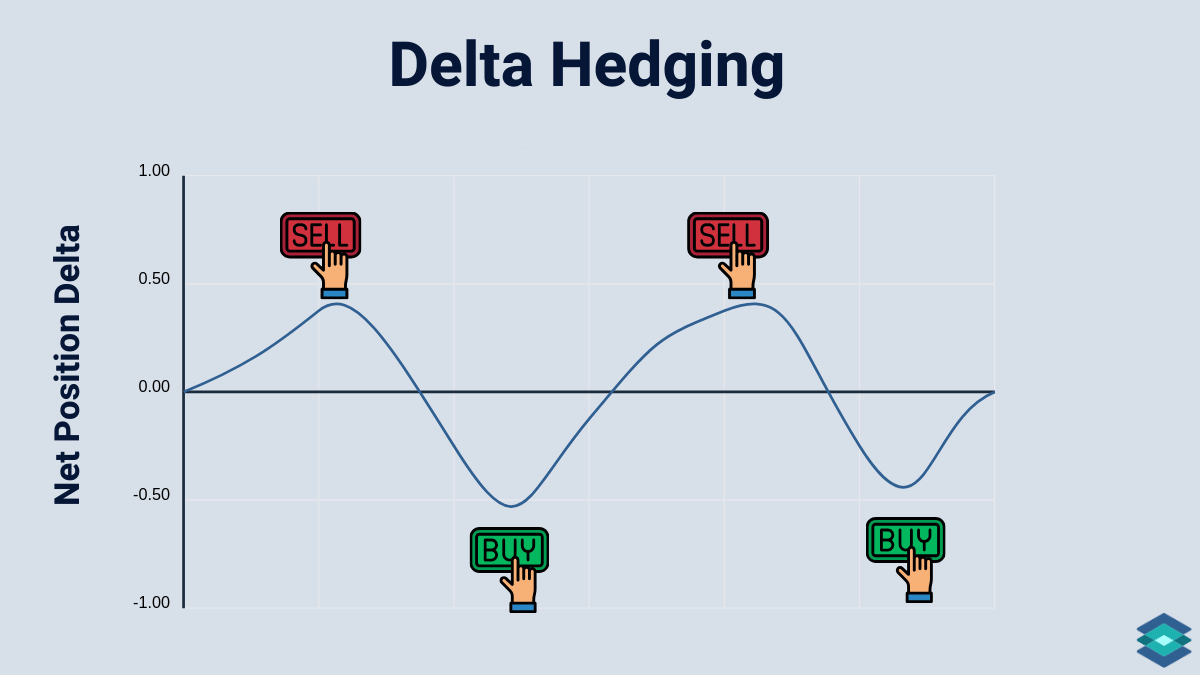

Adjusting the delta of an options position is actually quite simple - you simply buy or sell the underlying asset to bring the delta where you want it. For example, the below image shows a trader buying and selling in order to achieve a delta-neutral position. Let’s explore this in more detail below. You can also add or reduce option positions to adjust delta.

Delta Hedging in Options Trading

Delta hedging is a strategy that traders use to mitigate risk. The goal here is to have a ‘delta neutral’ portfolio, which is another way of sayin having no direction exposure. Here’s how it works.

- A trader notices that their net delta for a given underlying asset is running too high or too low. Too many positive deltas imply a very bullish position, while negative deltas imply a very short position.

- To reduce this direction risk, the trader will buy enough stock (offsetting short delta) or sell enough stock (offsetting long delta), to achieve a delta neutral position. Traders can also buy or sell options to offset excessive delta.

- The trader constantly monitors the position and readjusts once the delta falls outside their range.

Delta hedging is also a great risk mitigation strategy around high-volatility events, such as earnings. Rather than exiting an entire option position, the trader can hedge this risk with stock. However, this process requires much diligence and constant adjustment and is best suited for very active traders.

Explore Options With Virtual Trading

With TradingBlock’s Virtual Trading platform, you can trade options in a simulated environment. Check it out below today!

📖 Read Next: Option Gamma: The Greeks for Beginners

⚠️ Besides the initial premium paid, it is essential to consider the commissions and fees associated with most options transactions when calculating net profit or loss. These fees can significantly impact the overall return on investment and should be factored into all trades placed.

FAQ

A "good" delta in options depends on your specific strategy. If you’re really bullish, you’ll want a high positive delta. If you’re bearish, you’ll aim for a negative delta. It’s all about matching delta with your market outlook.

A positive 0.30 (or "thirty") delta means your option behaves like owning 30 shares of stock. A negative delta of -0.30 means the position acts like being short 30 shares of stock.

If a call option has a 10 delta (+0.10), it behaves like owning 10 shares of stock. It also indicates the option has roughly a 10% chance of expiring in-the-money at expiration.

At-the-money (ATM) options have a ±0.50 (fifty) delta because they have a 50% chance of expiring in-the-money.

Call options can’t have a negative delta, but they can have a zero delta, which means they’re very far out-of-the-money with almost no chance of expiring in-the-money. Put options, on the other hand, have deltas between 0 and -1, as these options have an inverse relationship with stock price.

In options trading, a negative delta implies a position profits when the underlying asset falls in price.

Delta gap shows the difference in delta between two options. A small delta gap implies less directional risk, while a large delta gap indicates higher sensitivity to price moves.

A single option with a delta of 0 means it’s far out-of-the-money, with almost no chance of expiring in-the-money. If an entire options position has a net delta of zero, it means the position is delta-neutral.

Yes, all put options have a delta between 0 and -1.

.png)