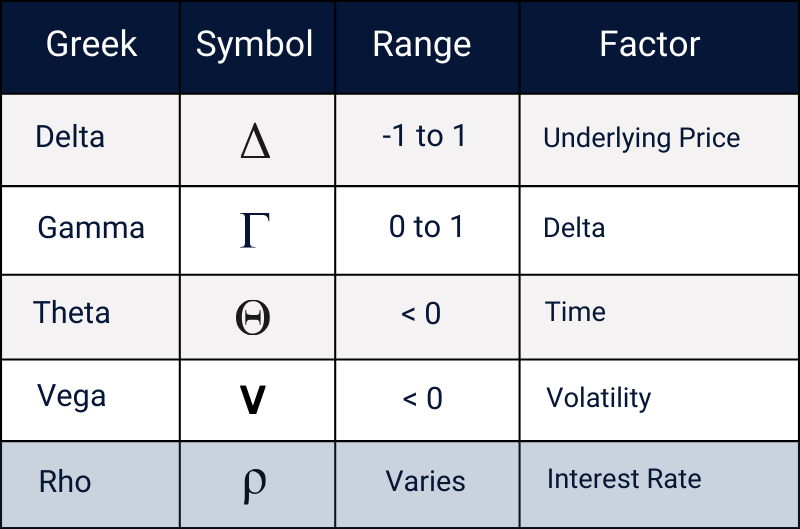

Option Gamma Explained: The Greeks for Beginners

Gamma measures how the delta of an option changes relative to a $1 change in the underlying asset's price. Long options always have a positive gamma, which ranges from 0 to 1.

.png)

The options Greek gamma measures how much an option's delta changes with a $1 move in the underlying asset's price. For example, if an option has a gamma of 0.05, a $1 move in the underlying asset will increase or decrease the delta by 0.05. Gamma can be thought of as the delta of the delta.

It is very, therefore, very difficult to understand gamma without first understanding delta. Lucky for you, we’ve written a comprehensive article on delta. 👇

Highlights

- Gamma measures the change in an option's delta resulting from a $1 change in the stock price.

- Delta is the 'speed' of an option's price movement relative to changes in the underlying asset's price, while gamma is the 'acceleration'.

- Long positions = positive gamma → Benefit from large price movements.

- Short positions = negative gamma → Suffer from large price movements.

Gamma & Delta Explained

I like to think of gamma as the horsepower of an option. The more gamma a particular option has, the more power it has to move the price of an option (in either direction).

Delta and Gamma can also be thought of, respectively, as speed and acceleration.

Delta measures how quickly an option's value changes in response to a stock price move, while Gamma shows how fast that speed (delta) increases or decreases.

As a reminder, the option Greek delta tells us how much the price of an option will move if the price of the underlying assets goes up or down by $1.

Delta also tells us:

- How many shares of stock an option trades like

- The percent chance an option has of expiring in-the-money

📉 What is Vega and How Does it Work?

Gamma Example

In order to understand how gamma and delta work together, let’s take a look at an example. We’ll start by isolating delta.

The first call option in the table below has a delta of 0.60, so this option will increase by 0.60 when the underlying rises in value by $1 and fall by 0.60 when the option falls by $1.

After the stock moves by $1, a new delta is assigned to the option, as shown on the table's far right side.

Gamma measures the rate of change in an option's delta for every $1 move in the underlying stock. For example, if a call option's delta increases from 0.60 to 0.65 when the stock price rises by $1, the gamma is 0.05. This shows how sensitive the option's delta is to changes in the underlying asset.

Let’s now take a look at the same table with gamma added.

Notice how gamma is always positive, even for put options with a negative delta? Let’s learn why next.

🧮 Check out our Option Greeks Calculator here!

The Range of Gamma

For long options, gamma ranges from 0 to +1, though a gamma above 0.20 is rare (more on this in our examples later).

Gamma is always the highest for at-the-money (ATM) options.

ATM options have the highest gamma because very small movements in the underlying asset can dramatically change the odds of ATM options expiring in-the-money (ITM) or our-of-the-money (OTM).

As we get further away from ATM options, there is more certainty surrounding the likelihood of the option expiring ITM or OTM. This lowered uncertainty causes the delta to change very slowly, resulting in lower gamma.

It is very common for deep ITM and far OTM options to have gamma’s of 0 because the likelihood of the option's outcome is almost certain, leaving little room for delta adjustments.

Option Gamma: Call vs Put Options

- Long call options have positive deltas and positive gamma.

- Long put options have negative deltas and positive gamma.

The delta of all long call options is between 0 and 1, while the delta of all long put options is between 0 and -1. Gamma is always positive (or zero) for all long options.

So why is gamma always positive on option chains? Because this Greek measures the rate of change in delta, not the direction.

Gamma vs Time

Gamma has a dynamic relationship with time. As option expiration approaches, gamma grows for at-the-money (ATM) options, while in-the-money (ITM) and out-of-the-money (OTM) options often experience significant gamma decay.

The below visual graph shows the real-world gamma of SPY (SPDR S&P 500 ETF Trust) call options over three different expiration cycles.

Here are two observations regarding the above visual:

- Flat Gamma for 17 DTE: With 17 days to expiration, options have a lot of time value, so delta changes very little here, resulting in low and flat gamma across strike prices.

- Gamma at 0 DTE Drops to Zero: At expiration, ITM options behave like the underlying stock (delta near ±1), while OTM options, with little chance of moving in-the-money, lose sensitivity. With no further changes in delta possible, gamma drops to zero.

Gamma vs Implied Volatility

Gamma has an inverse relationship with implied volatility.

When implied volatility increases, options prices rise. This results in higher extrinsic value. This reduces gamma because changes in the underlying price have less impact on the option's delta when there is a lot of extrinsic value remaining.

On the flip side, when implied volatility decreases, gamma increases as the option's price becomes more sensitive to changes in the underlying.

What is Short Gamma?

So far, we have looked only at long options. We learned that gamma is positive for long options, regardless of whether that option is a call or put. This changes with short options.

All short options have negative gamma. This is because the delta changes in the opposite direction of the stock price movement

Short Gamma Example

You can’t see short gamma on an options chain - you can only see it when you create a ‘position’ in an underlying asset. If you were to sell short an option and then check your ‘position,’ you would see the ‘position gamma’ is negative.

Let’s take a look at an example. This should be pretty intuitive as it is simply the inverse of what we learned earlier.

Let’s examine the first row of the table. The short call position starts with a delta of 0.6 and a gamma of -0.05. When the stock price rises by $1, the delta decreases to 0.55, and when the stock price falls by $1, the delta increases to 0.65.

This negative gamma is significant because it causes the position to become increasingly short (higher delta) as the market declines and less short (lower delta) as the market rises.

📖 Long vs Short Gamma: How They Differ

Short Call: Gamma and Payoff

The chart below illustrates the relationship between profit/loss (P/L) and gamma for a short call option with a strike price of 100.

Why Does Gamma Matter?

The greatest benefit of gamma is that it measures how much an option's delta will change for a $1 move in the underlying price. High Gamma means the option's sensitivity to price changes increases rapidly, making ATM options the most responsive. In contrast, low Gamma indicates more stable delta changes, with smaller adjustments as the underlying shifts.

Buying options with high gamma can help you take advantage of large price moves in the underlying asset, as these options will see faster delta changes and more pronounced gains when the price moves in your favor.''

On the flip side, selling options exposes you to short gamma risk. This means that as the underlying price moves, the delta of your position will change unfavorably, requiring continuous adjustments to remain hedged.

Gamma and Option Strategies

As we learned, all long options have positive gamma, and all short options have negative gamma.

When you have a position that includes both long and short options, your net gamma will tell you the overall sensitivity of your position's delta to changes in the underlying price.

A positive net gamma means your position benefits from price movement, while a negative net gamma means large price moves will work against you, increasing risk.

Here are a few different option strategies and their respective gamma profiles.

What is Gamma Hedging?

- Delta Hedging: Reduces risk from stock price movement by using a stock or option hedge, focusing more on changes in volatility.

- Gamma Hedging: Refers to the adjustments made to delta hedges (e.g., daily, weekly) to account for changes in stock prices, maintaining the effectiveness of the hedge.

A portfolio with too many positive or negative gammas can experience volatile swings in delta as the underlying asset price moves. Many traders use gamma hedging strategies to offset this risk.

While delta hedging can be done by buying/selling the underlying assets or options on that asset, gamma hedging is done purely through options.

For example, if your gamma risk is skewed positively because you have too many calls, adding put contracts will help neutralize the gamma exposure by offsetting the sensitivity to price changes in the underlying asset.

A gamma-neutral portfolio means your position has no sensitivity to changes in the rate of delta as the underlying price moves. Maker makers, who often have vast inventories of options, often try to achieve a gamma-neutral portfolio to offset the risk of large price swings.

What is a Gamma Squeeze?

A gamma squeeze occurs when a very large move in the price of the underlying asset forces market makers to buy or sell large amounts of the asset to hedge their open options positions.

Whenever you buy an options contract, a market maker typically takes the other side of that trade. For example, if you were to buy a 0DTE call on a meme stock, which we’ll call ABC, a market maker will have sold you that call, leaving them with upside risk exposure.

To neutralize this risk, a market maker may buy the underlying stock as the price increases to hedge their short-call position. As the stock price rises, the market maker must buy more shares to maintain a neutral delta, which can amplify the upward price movement, creating a gamma squeeze.

Gamma: Live Trading Example

Let's conclude by taking a look at the gamma for a SPY options chain on the TradingBlock platform. These options expire in one day.

.png)

You should be able to spot a few things we learned in this article, such as:

- ATM Options and Gamma: At-the-money (ATM) options have the highest gamma.

- ITM and OTM Gamma Behavior: Deep in-the-money (ITM) and out-of-the-money (OTM) options have very low gamma values, particular for the options on this chain, which expire in 1 day.

Explore Options Trading With Virtual Trading

With TradingBlock’s Virtual Trading platform, you can trade options in a simulated environment. Check it out below today!

⚠️ Besides the initial premium paid, it is essential to consider the commissions and fees associated with most options transactions when calculating net profit or loss. These fees can significantly impact the overall return on investment and should be factored into all trades placed.

FAQ

A good gamma for options will depend upon your market outlook and options strategy. High gamma is great for short-term traders looking to profit from large swings in the price of a stock, while low gamma is best suited for traders looking to profit in a market-neutral environment.

High gamma is a good strategy for traders looking to profit from large price moves, as it increases the option's sensitivity to changes in the underlying asset.

All long options, both calls and puts, have long gamma, while all short options have short gamma.

A gamma squeeze occurs when market makers hedge short call positions by buying shares of the underlying asset, which drives the stock price up.

Gamma risk occurs when a position has high gamma exposure, meaning the position's delta is highly sensitive to price moves in the underlying asset. This can lead to large, unpredictable changes in the option's value as the underlying price fluctuates.

.png)