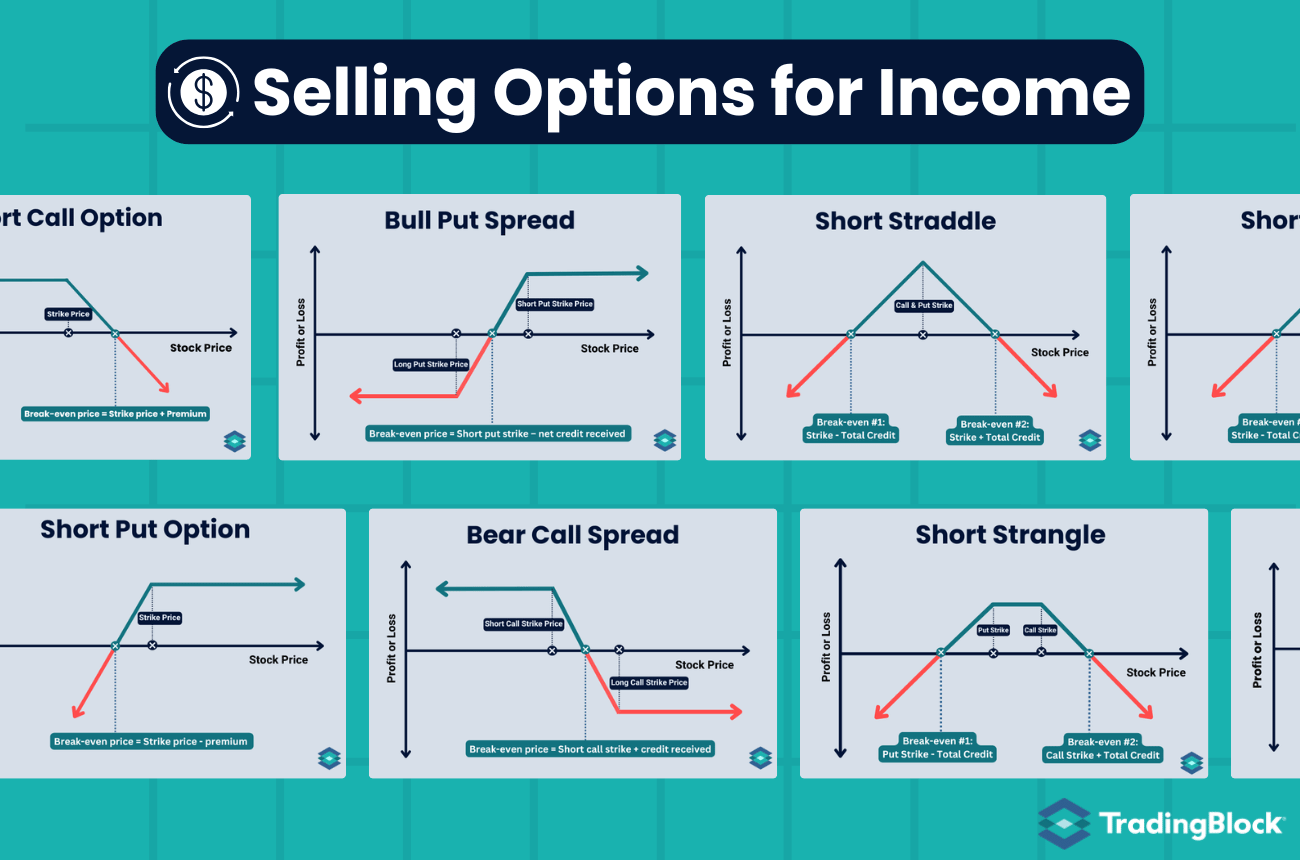

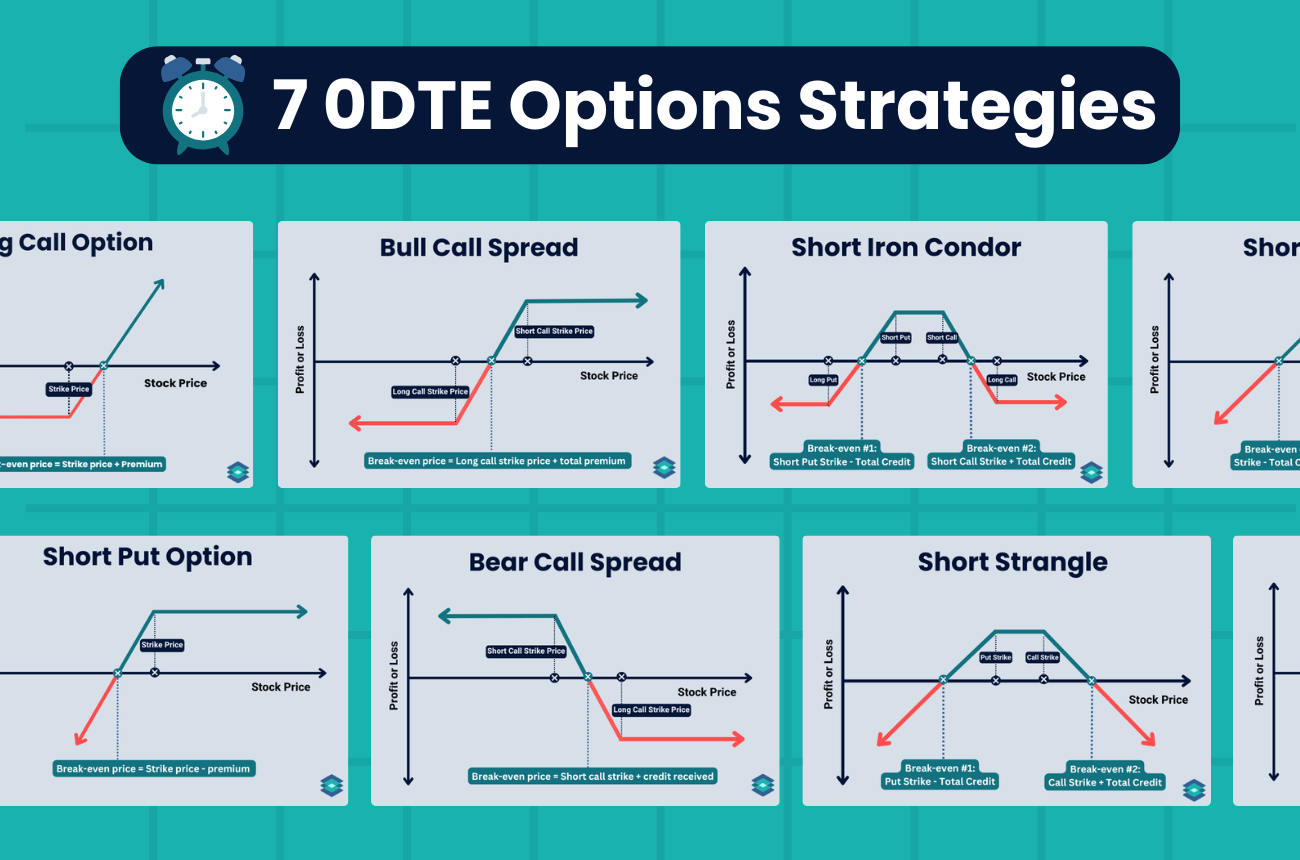

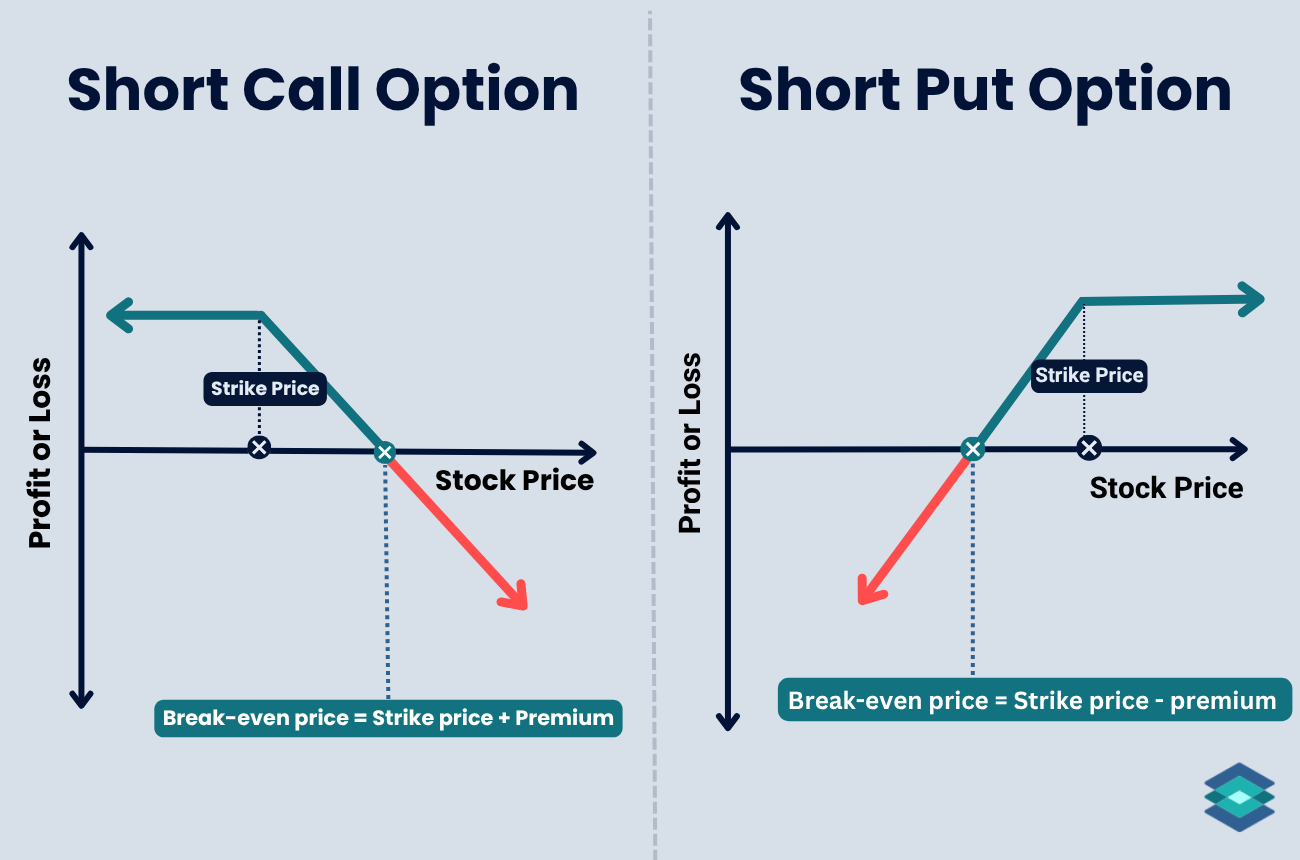

0DTE Options: 7 Strategies And When To Use Them

This article breaks down seven core 0DTE options strategies, including long calls and puts, credit spreads, and iron condors.

This guide explores how to trade 0DTE options across a range of strategies, from speculative longs to high-probability premium selling. It also explains when each setup works best and what to watch for as expiration nears.

Highlights

- 0DTE options expire the same day they’re traded and are either listed that morning or simply reach expiration after a longer life, with the latter typically offering better liquidity.

- Risk is amplified on 0DTE trades, especially from gamma swings, time decay, poor execution, and low liquidity.

- Buying single options is high risk/high reward, especially if volatility is expected or if gamma is elevated near the money.

- Selling spreads or condors can offer high probability setups, but require disciplined sizing and close monitoring, especially late in the day.

- Short straddles and strangles offer premium-rich trades, but come with undefined risk and demand constant attention as expiration nears

0DTE Options Overview

Zero days to expiration (0DTE) options expire on the current trading day. There are two varieties of 0DTE options:

- Options that expire on the same day they are issued (newer to market)

- Longer-dated options that happen to expire on the current trading day (more established)

The latter generally offer better liquidity since they’ve been trading for a longer period. In contrast, same-day listed 0DTE options are newer and can be less liquid, especially early in the session.

Zero days to expiration options are particularly popular among retail traders and continue to grow rapidly. According to the Chicago Board Options Exchange (CBOE), 0DTE options on the SPX index have increased fivefold over the three years ending in 2025.

In this article, we’ll help take the guesswork out of 0DTE trades by breaking down when you should use different strategies, how to spot opportunities, and which setups give you a fighting chance.

But first, we’re going to cover the basics:

4 Risks of 0DTE Options

0DTE options can be incredibly risky. This assumes you're using these options for speculation and not hedging, which is how most retail traders use them. Their high-risk nature is exactly why they’re so popular.

Here are four risks to watch for:

- Liquidity risk is a particular concern for 0DTE options, especially when they first begin trading, since volume and open interest are often low.

- Gamma risk is huge with 0DTE options because delta can swing sharply with even small price movements, especially when the option is near the money. This makes it difficult to manage positions since gains can vanish or losses accelerate in a matter of seconds.

- Execution risk is also real with 0DTE options. You may only have seconds to lock in profits or cut losses, and poorly placed orders (or fills) can make the difference between a winner and a loser.

- Time decay (theta) risk is also a major risk for net debit positions (like long calls or puts) on 0DTE options. To understand why, it helps to first look at how option pricing works.

Understanding Option Value

.png)

Because they expire on the day they are traded, 0DTE options are typically very cheap compared to options with more time until expiration. This is because most of the extrinsic value, or time value, has already been drained from the premium.

An option’s price is made up of two parts:

- Intrinsic Value: The amount an option is “in the money” by

- Extrinsic Value: The portion of an option’s price that reflects time value, driven by time remaining until expiration and implied volatility.

Let’s jump right to an example to understand better.

Intrinsic vs Extrinsic Value Example

ABC is trading at $100, and we own the 103 call. Here’s how its extrinsic and intrinsic value may look on 3DTE and 0DTE:

2 Days to Expiration:

- Stock Price: $100

- Strike Price: 103 (out of the money)

- Intrinsic Value: $0

- Extrinsic Value: $0.40

- Total Option Price (Premium): $0.40

Morning of Expiration (0DTE):

- Stock Price: $100

- Strike Price: 103 (still out of the money)

- Intrinsic Value: $0

- Extrinsic Value: $0.05

- Total Option Price (Premium): $0.05

On the morning of expiration, most of the option's value has decayed away. Unless ABC rallies above 103 before the market closes, the option will expire worthless. The odds of this option expiring worthless are incredibly high.

However, if a sudden catalyst triggers a rally through the $103 strike price, which is not uncommon in 2025’s volatility, the option could deliver outsized returns. After all, you only paid $0.05 for the long call.

This is why I often compare buying 0DTE options to buying lottery tickets. If you have a big risk appetite and do not mind the mental stress of watching your long option decay in real time, trading single 0DTE options might be for you.

7 0DTE Option Strategies

In the sections below, we’ll walk through seven 0DTE options trading strategies, and, most importantly, the types of market conditions where each one may be effective. The goal is to introduce more structure to your trading and remove some of the emotion from the process.

1. Buying Single Calls and Puts

.png)

Buying single call or put options (going long naked, as we call it in the business) is one of the most popular 0DTE strategies among retail traders. Many inexperienced traders randomly choose a cheap out of the money option and send off the trade without a plan. That’s not much different from gambling.

But there can be some strategy here. Your first step should be to head over to your TradingBlock dashboard and locate ‘delta’ on the options chain. This option Greek tells us a few things:

- How much the option is expected to move for a $1 move in the underlying asset

- How many shares of stock the option ‘trades like’

- The percent chance that an option has of expiring in the money

We’re going to focus on the last bullet here. Since we want our long call or put to expire in the money, we want the delta to be high, and ideally, the price to be very low. Let’s jump right to an example to see delta in action:

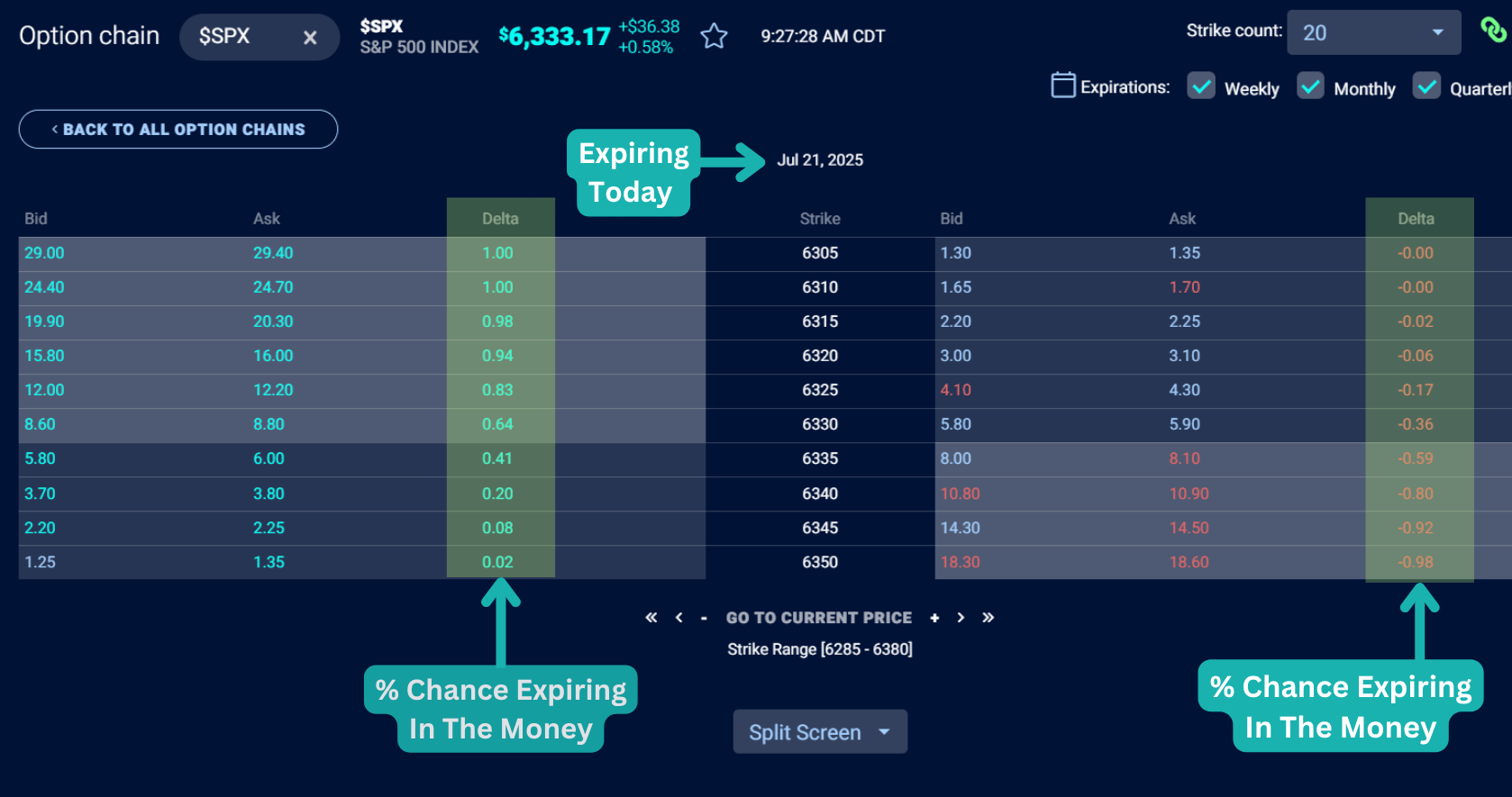

0DTE Single Option Example: Delta

Here is a live TradingBlock options chain for options expiring today, in 6 hours, on SPX (S&P 500 Index):

If we look at the out of the money 6350 call, we can see it's trading around $1.30 at the mid-point. The delta is just 0.02, which tells us a few important things:

- That’s only a 2% chance of expiring in the money

- You're paying $1.30 (or $130) for an option with a 98% chance of expiring worthless

Even if it does land in the money, you still need an extra $1.30 move to break even. In this case, SPX would need to rally about 0.80% to reach 6351.30 (strike plus premium). Not impossible in this kind of volatility, but still a pricey bet.

When To Buy 0DTE Single Options

Here are a few examples of when buying a single 0DTE option can be a calculated decision and therefore make sense:

- When implied volatility is low but a known event is coming: Like right before an economic announcement on tariffs from the current administration.

- When far out of the money options show heavy volume: For example, if our previous 2% delta call suddenly sees a spike in volume, it may hint at bets or hedging setups that could pull the market toward that strike.

- When gamma is high near the money: These strikes react fastest to price changes. A small move in SPX can create big shifts in option value, and dealer hedging may accelerate it. You can find current gamma levels on your TradingBlock options chain.

- After a sharp market move, when you expect a reversal: Market makers often hedge long gamma positions in the opposite direction of price. That hedging pressure can cause snapbacks, giving you a shot with a call or put.

- When today’s option volume far exceeds open interest: This shows new positions being built, which can increase the odds of dealer hedging flows impacting SPX intraday.

📖 SPX vs SPY Options: 7 Major Differences

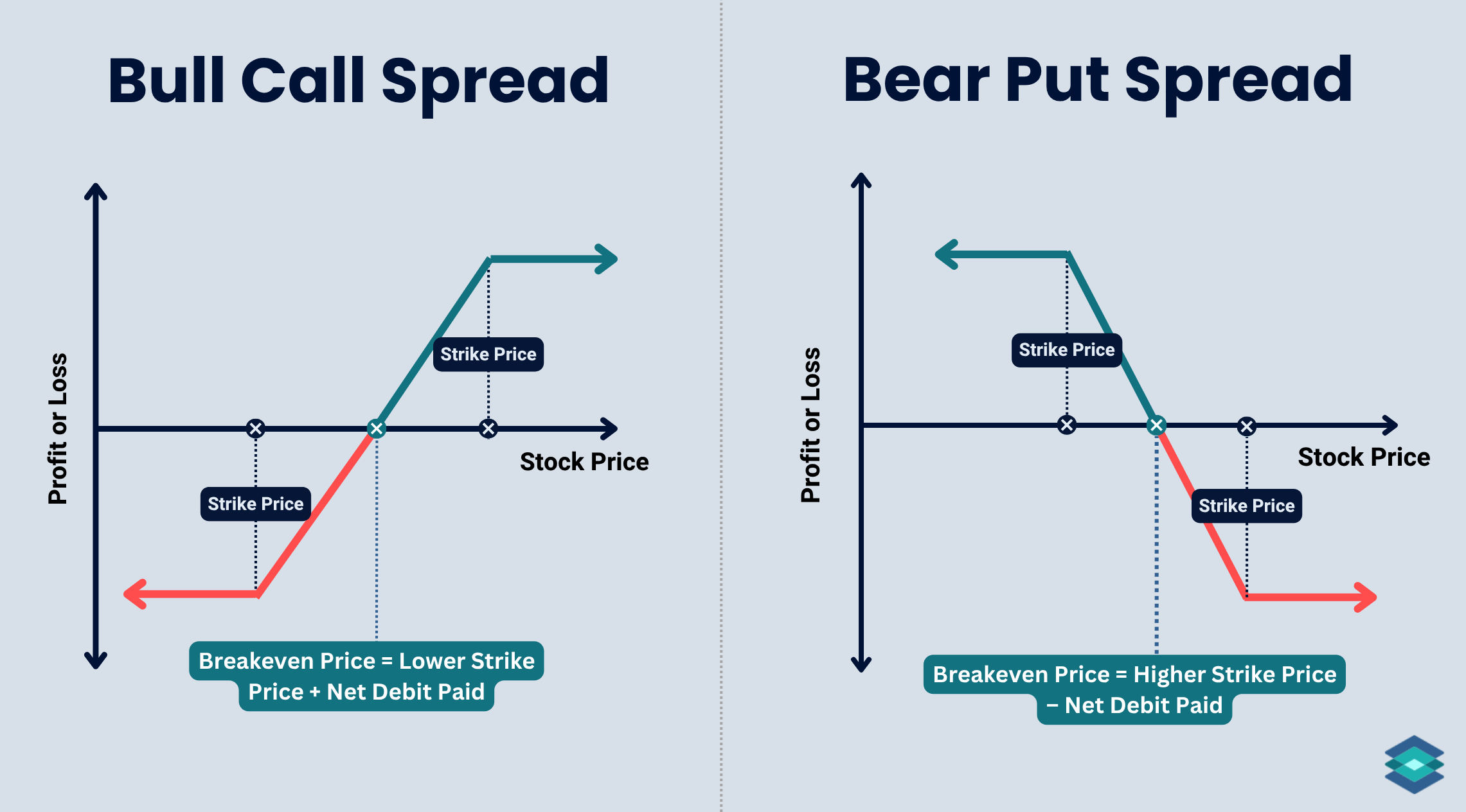

2. Buying Vertical Spreads

There are two types of long vertical spreads:

- Bull Call Spread (bullish)

- Bear Put Spread (bearish)

Both strategies involve buying an option close to the money and selling another option further out of the money. These are debit spreads, which means you pay to enter the trade. You're long volatility, hoping for a significant move in your direction.

Even though these strategies are very popular, they are not my favorite. That’s because the maximum profit is capped at:

- Spread Width – Debit Paid

If I’m going to take a swing on a net debit 0DTE options trade, I’m swinging for the fences with a single call or put. Let’s look at an example to see why:

0DTE Bull Call Spread Example

Let’s say XYZ, a high-beta tech stock with a major announcement expected before the close, is trading at $100 with two hours until expiration.

You enter a 0DTE bull call spread by buying the at the money $100 call and selling the $102 call, paying $0.75 for the spread. Since the spread width is $2.00, your max profit is $1.25.

Now suppose XYZ rallies and closes at $105. Let’s compare the payoff from our long call spread and just the long 100 call option unhedged:

Bull Call Spread ($0.75 cost):

- Max value at expiration: $2.00

- Profit: $2.00 – $0.75 = $1.25

- Return: 167%

Long $100 Call ($1.25 cost):

- Final value at expiration: $5.00

- Profit: $5.00 – $1.25 = $3.75

- Return: 300%

So yes, the spread limits your risk, but it also limits your upside. If you’re trading 0DTE options and aiming for a big move, that cap can be frustrating. Spreads can also be incredibly wide as expiration approaches, eating into your profits.

When To Buy 0DTE Vertical Spreads

Here are a few instances where buying vertical spreads on 0DTE may make sense.

- Time decay relief: Single-leg options lose value quickly on 0DTE, but spreads help reduce decay by selling premium and lowering the breakeven.

- Mild directional bias: You expect a move but not a massive one, so you limit risk and reduce cost compared to buying a single option.

- Rich premiums: Implied volatility is high and options are expensive, so using a spread reduces your exposure to a volatility crush.

- Crowded strikes: When volume builds around a key level, buying a spread slightly above or below that range can help you play the momentum or fade it.

3. Selling Vertical Spreads

.png)

If you take the other side of the two strategies we just covered, you get two of the more popular net credit spreads:

- Bear Call Spread (neutral to bearish)

- Bull Put Spread (neutral to bullish)

In both cases, we want the underlying to stay near or move away from the short strike. Since we’re net short options, time decay works in our favor on these trades, and they generally have a higher profitability percentage than debit spreads.

Back when I was an options broker, selling vertical spreads was the go-to strategy. We often sold them during the final week of expiration (sometimes on expiration day) because that’s when time decay accelerates most.

Traders often targeted returns of around 5 percent on these spreads. While that might sound modest, consider you’re only in the trade for a few hours. When you’re selling out of the money spreads, or even close to the money spreads, the probability of profit is generally high.

Let’s look at an example:

0DTE Short Vertical Spread Example:

Here’s an example short put spread on SPX. We’re going to say SPX is trading at 6,300 right now to keep things clean. Implied volatility is through the roof due to tariff uncertainty, which means option prices are inflated far more than usual. This can be a great time to sell premium, if you know what you're doing and understand the risks.

Here is our trade:

- SPX Price: 6,300

- Sell the 6,250 put for: $0.65

- Buy the 6,240 put for: $0.10

- Net credit: $0.55

- Max loss: $9.45

- Max gain: $0.55

You're risking $9.45 to make $0.55, targeting a 5.8% return in a single day. If SPX stays above 6,250 at expiration, you keep the full credit.

But beware: while this trade may win most of the time, a single loss can erase multiple prior winning trades. This is a 10-point spread, which is quite wide and risky, especially since we’re only taking in $0.55.

Sizing and discipline matter, especially when trading 0DTE options.

When To Sell 0DTE Vertical Spreads

Here are a few market environments that may be conducive to selling 0DTE vertical spreads:

- When markets are calm and range-bound: These conditions reduce the chance of sudden moves breaching your spread.

- When implied volatility is slightly elevated: You collect more premium without exposing yourself to chaotic swings.

- When you can manage the position intraday: Many traders open short spreads in the morning and close them before the final hour to avoid late-day whipsaws.

- When you’re sizing properly: These setups offer small gains relative to large risks, so position size is everything.

4. Selling Iron Condors

.png)

A short iron condor combines both a bull put spread (short put spread) and a bear call spread (short call spread). It’s a great way to take advantage of options’ rapid time decay on expiration day while keeping your risk defined.

You’re selling both of these spreads at the same trade, aiming to profit from time decay and a market that stays in a range.

- Sell a call spread above the market

- Sell a put spread below the market

If both spreads expire worthless, you keep the entire premium. The trade works best in range-bound markets with slightly elevated implied volatility, where time decay can do the heavy lifting.

Your risk is defined. The most you can lose is the width of one spread minus the total credit received. But if the market moves sharply and breaches either side, you can hit max loss. Sizing and discipline are crucial.

0DTE Short Iron Condor Example:

In this example, we’re going to add a short call spread onto the 6250/6240 put spread from earlier. To be a true iron condor, the distance between strikes should be equal on both sides.

- SPX Price: 6,300

- Sell the 6250/6240 put spread for: $0.55 net

- Sell the 6350/6360 call spread for: $0.45 net

- Net credit: $1.00

- Max loss: $9.00

- Max gain: $1.00

- Breakeven range: 6249 to 6351

- Profit range: SPX finishes between 6250 and 6350 at expiration

The iron condor is great because it essentially doubles your profit potential compared to selling just one side of the trade. But it also increases your exposure. You're now at risk on both sides of the market.

If the call and put spreads are sold equal distance out of the money, your chance of getting tested goes up. Your max loss is still capped, but you're playing defense in both directions.

Personally, I like to leg into iron condors. If I sell a call spread and the market pulls back a bit, I’ll then sell the put spread on the other side to complete the condor. That way, I collect more premium and improve my breakeven range while reacting to price action rather than guessing both sides up front.

When To Sell 0DTE Iron Condors

Here are a few setups where selling iron condors on 0DTE options may make sense:

- When the short strike delta is around 0.15: Each side has about an 85% chance of expiring worthless, with a combined profit probability near 70% and higher premium to match the added risk.

- When there is still decent premium left: You don’t want to wait too long in the day because there won’t be much premium to sell. Aim for mid to late morning.

- When you can actively manage the trade: Gamma risk peaks in the final 30 minutes, and it's even higher here if you're short two spreads that aren't too far out of the money. Watch closely or consider closing out before that window.

- When the market is calm or range-bound: Avoid placing spreads near big economic events or known catalysts.

- When IV is slightly elevated but not spiking: You want to sell rich premium without walking into a volatility explosion.

5. Selling Single Options Naked

Selling naked options is a high-probability but high-risk way to trade 0DTE options. It is a straightforward method of taking advantage of time decay, but is best reserved for seasoned traders. You don’t want to learn by selling options naked, I assure you.

You have two options:

- Short naked put: You are betting the market stays above your strike.

- Short naked call: You are betting it stays below.

Most professional traders lean toward selling out of the money naked puts. This is because volatility tends to spike on the downside, which inflates option premiums. More volatility means more extrinsic value to sell.

One advantage of selling options on 0DTE options is that your option margin is only tied up for a few hours. This is in contrast to longer-dated options, where you really have to consider the opportunity cost of that capital being locked up and unavailable for other trades.

Know Your Greeks

Before entering a naked short trade (or the short strategies that follow in this article), it’s essential to understand the option Greeks. Start with delta. As we mentioned earlier, this Greek gives you a rough idea of the probability your option expires in the money. Use that number to weigh the risk against the premium you’re collecting. Is the trade worth the risk? Remember, for a short call, the risk is infinite.

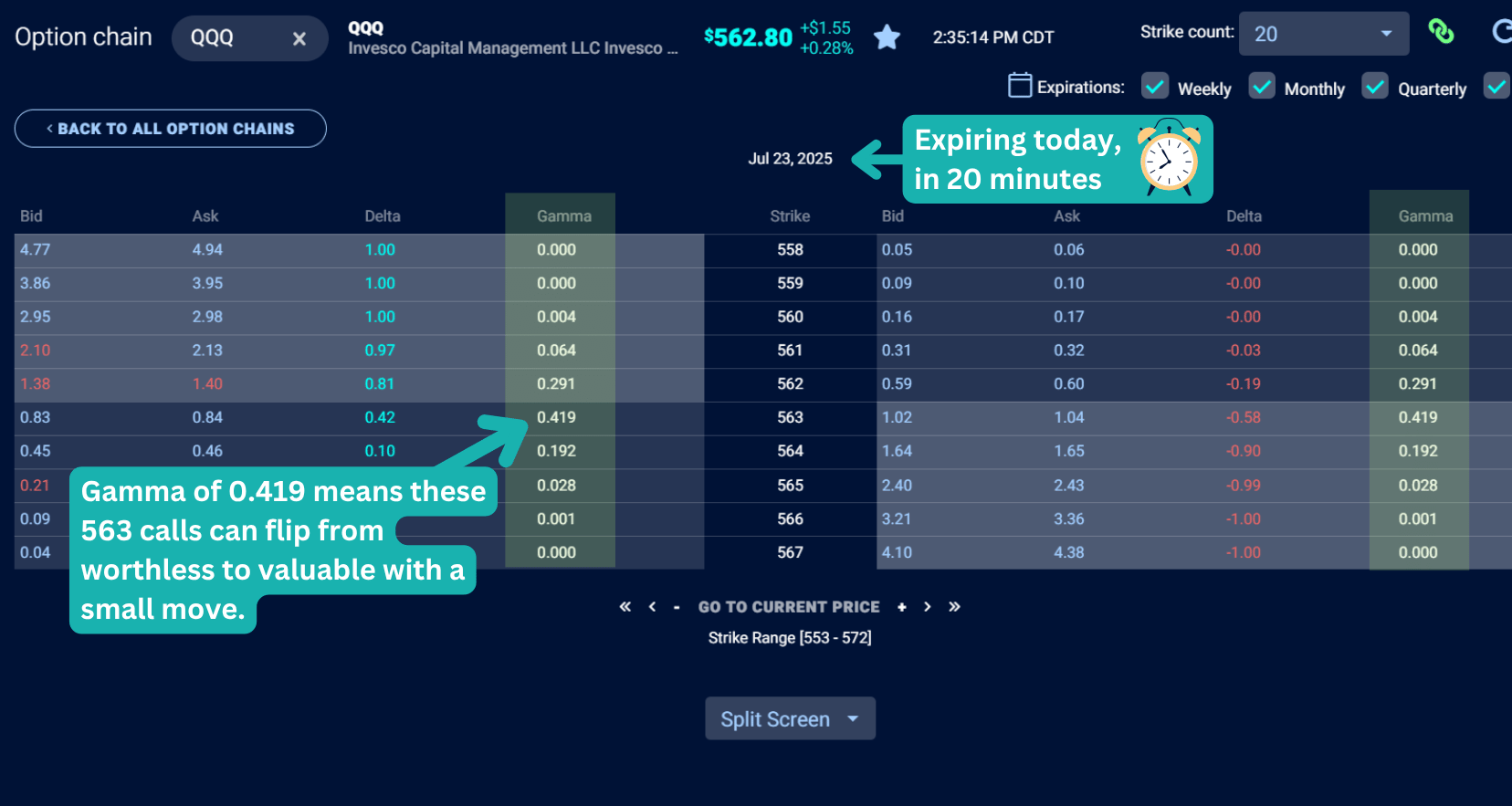

Once the trade is on, shift your focus to gamma. With 0DTE, gamma risk is extreme. A small move in the underlying can flip your position fast. What looks safe in the morning can be deep in the money by the close.

Let’s head back over to the TradingBlock dashboard and look at the gamma on some options expiring in only 20 minutes:

0DTE Naked Option Example

In this example, we will say that SPX is currently trading at 6,300. We’re going to sell the 6,250 put. Implied volatility is still very much elevated, so we’ll collect some nice premium:

- SPX at entry: 6,300

- Sell the 6,250 put for $0.90

- Max profit: $90

- Breakeven: 6,249.10

- Max loss: undefined

- Profit if SPX stays above: 6,250 at expiration

Now let’s say everything is going according to plan - until the final 15 minutes of trading, when news breaks of new trade restrictions on Europe. The market tanks, and SPX drops hard:

- SPX falls from: 6,250 → 6,174 (–2%)

- 6,250 put settles at: intrinsic value of 76 points

- Closing price of put: ~$76.00

- P&L: You sold the put for $0.90, now worth $76.00

- Loss: $76.00 – $0.90 = $75.10 x 100 = $7,510 loss

That’s a huge loss considering our maximum profit was only $90. You'd need 84 winning trades in a row at $90 profit each just to recover one $7,500 loss!

In fast markets, managing positions can be nearly impossible. And when you try, bid/ask spreads can get so wide that your fills are horrendous. Stop orders won’t save you in these markets either. I have seen $5 sell stop orders filled at $0.10 intraday!

When To Sell 0DTE Naked Options

For you risk takers, here are a few setups when selling naked options on 0DTE may make sense:

- When the short strike delta is under 0.15: That suggests about an 85% chance of expiring worthless, but odds can actually be higher at trade entry because delta doesn't fully account for rapid intraday time decay and decreasing volatility.

- When volatility is high and premium is rich: You’re taking real risk, so the reward better justify it. Richer premium gives you a bigger cushion.

- When you’re trading small and sizing right: The best naked traders use small size. One big loss can wipe out a string of wins.

- When you’re glued to the screen: Gamma ramps up into the close. If the market whips, you’ve got to be ready to close or roll fast.

- When there’s no major event on deck: Avoid naked trades ahead of big data, FOMC, or earnings. A calm market can turn chaotic in seconds.

- When you’ve got a system, not a hunch: Define your exits, profit targets, and max pain before entering.

6. Selling Straddles

.png)

The short straddle options strategy consists of selling two at the money options at the same strike:

- Sell a call at the money

- Sell a put at the same strike

You’re betting the underlying stays close to the strike through expiration. Time decay is your friend, and if both options expire worthless, you keep the full premium. However, this hardly ever occurs because it would mean the underlying has to pin your strike price at the moment of expiration. You will not likely reach max profit on this trade.

Since straddles are sold at the money (and assuming the underlying is trading at that exact strike price), each leg will have a delta around 50, implying about a 50% chance of expiring in the money.

But only one option can finish in the money at expiration, not both. And because we collected premium on both sides, our actual odds of turning a profit are slightly better than 50%.

But make no mistake: this is a risky trade. You’re exposed on both sides, and if the underlying makes a big move in either direction, losses can mount quickly. Let’s take a look at an example:

0DTE Short Straddle Example

In this example, SPX is trading at 6,300, and the options we’re trading will expire in just 3 hours. Here are our trade details:

- SPX price at entry: 6,300

- Sell the 6300 call for: $7.20

- Sell the 6300 put for: $6.80

- Total credit received: $14.00

- Max profit: $14.00

- Max loss: Unlimited

- Breakeven range: 6,286 to 6,314

In this outcome, SPX rallied modestly going into the close, settling at 6,310:

- SPX: 6300 → 6310

- 6300 call: $7.20 → ~$10.00

- 6300 put: $6.80 → $0.00

- Total value at expiration: $10.00

- Net gain: $4.00

The short straddle wins as long as SPX stays between the two breakeven points - in this case, roughly 6,286 and 6,314. A 10-point rally still lands inside the profit zone, and we keep a nice profit of $400.

When To Sell 0DTE Straddles

- When implied volatility is high: Elevated IV means richer premiums. This boosts your breakeven range and compensates for the straddle’s directional risk.

- On range-bound, low-news days: The trade works best when you expect little movement. Avoid major economic releases or Fed days.

- When the underlying is sitting near a key level: Big psychological or technical levels often act as magnets intraday.

- Mid-morning to early afternoon: You still collect solid premium, and theta starts accelerating.

- When you can actively manage it: You need to monitor this trade closely. Gamma risk near the close is no joke.

- When you’re comfortable with your position size: Straddles are naked both ways. Know your max loss is undefined, and position accordingly.

7. Selling Strangles

.png)

The short strangle is a high-probability, low-reward trade. It’s similar in structure (not payout) to the short straddle but involves selling an out of the money call and an out of the money put instead of at the money options.

- Short OTM Call – Betting the market stays below this strike

- Short OTM Put – Betting it stays above this strike

This trade is indeed high risk, but even though you’re selling two options, it’s actually less risky than selling a single naked option because:

- The premium is larger: You're collecting more upfront, which helps widen your breakeven range.

- The risk is spread: You’re not leaning entirely bullish or bearish. The trade is neutral, so you’re less exposed to a one-sided move.

Let’s jump right to an example:

0DTE Short Strangle Example

In this example, we will assume that ABC is trading at $100/share. We’re going to sell a strangle expiring in 5 hours that is 1% out of the money:

- ABC Price: 100

- Sell the 101 call for: $0.25

- Sell the 99 put for: $0.25

- Total premium collected: $0.50

- Upper breakeven: 101 + 0.50 = 101.50

- Lower breakeven: 99 – 0.50 = 98.50

- Net delta: ~0.00 (short call and put deltas mostly offset each other)

Since we’re short both an out of the money call and put with similar deltas, the net delta of the position is close to zero, meaning the trade is delta-neutral at entry.

When To Sell 0DTE Strangles

- When you expect range-bound price action: Ideal for low-movement days like post-earnings.

- When both short strikes have deltas near 0.10: This setup targets roughly an 80% probability of full profit.

- When you can monitor closely into the close: Gamma risk spikes in the final hour. Active management is key with short strangles.

- When there’s strong support and resistance nearby: Sell strikes just beyond key technical levels to help improve odds of expiring worthless.

- When premium justifies the risk: A wider breakeven zone with solid credit makes the trade more attractive.

ODTE: Option Greeks Summary

To wrap things up, here’s a table comparing how the Greeks affect net long versus net short 0DTE trades:

Trade 0DTE Options with Virtual Trader

New to options trading? Trade 0DTE options with our Virtual Trader platform! Learn options without risking real money.

⚠️ 0DTE (zero days to expiration) options are highly speculative and carry significant risk. These strategies are intended for experienced traders who understand options pricing, execution risk, and the impact of rapid time decay. The examples in this article are for educational purposes only and do not account for commissions, slippage, or tax considerations. Refer to The Characteristics and Risks of Standardized Options before trading.

FAQ

0DTE options are options that expire the same day they’re traded. They are generally high risk, high reward trades.

The best 0DTE options strategy depends on your market outlook. If you expect a big move, net debit strategies like long calls or puts may work. If you expect the market to stay put, selling premium can make take advantage of time decay. Think short puts, short iron condors, or short straddles.

Not long. These trades are fast-moving. Many traders manage them within minutes or hours. Holding until expiration can work, but it adds risk, especially with near the money options.

0DTE trading can drive intraday volatility. When large positions need to be hedged, especially around key price levels, it can amplify moves and create sharp reversals.

No. Options only trade during regular market hours. After the close, you can’t make any changes, so you need to manage your trades before the bell.

.png)

.png)

.png)