Protective Put Options Strategy: Beginner's Guide

The protective put strategy is a bullish options trade that pairs long stock with a put option to hedge against potential losses.

.png)

A protective put is a bullish options strategy where an investor buys a put option while holding the underlying stock to limit downside risk. It acts like insurance, setting a floor price the stock can be sold at if it drops in value.

Highlights

- Risk: Losses are capped below the put strike price, plus the premium paid. Once the stock drops past the strike, the put offsets further losses dollar-for-dollar.

- Reward: Upside is unlimited. If the stock rallies, the put expires worthless and you keep the gains, minus the cost of the hedge.

- Outlook: Bullish with downside concerns. Great for traders who want to stay long while protecting against short to medium-term drops or volatility events.

- Time Decay: Theta works against you. Out of the money puts steadily lose value, especially inside 30 DTE. I like to roll around that point to stay ahead of the decay.

- Defined Risk Hedge: Think of it like insurance. You pay a small premium to lock in a floor and avoid panic-selling during market drops.

🤔If you’re new to options trading, it helps a lot to understand how the long put option works before moving on to the protective put trade!

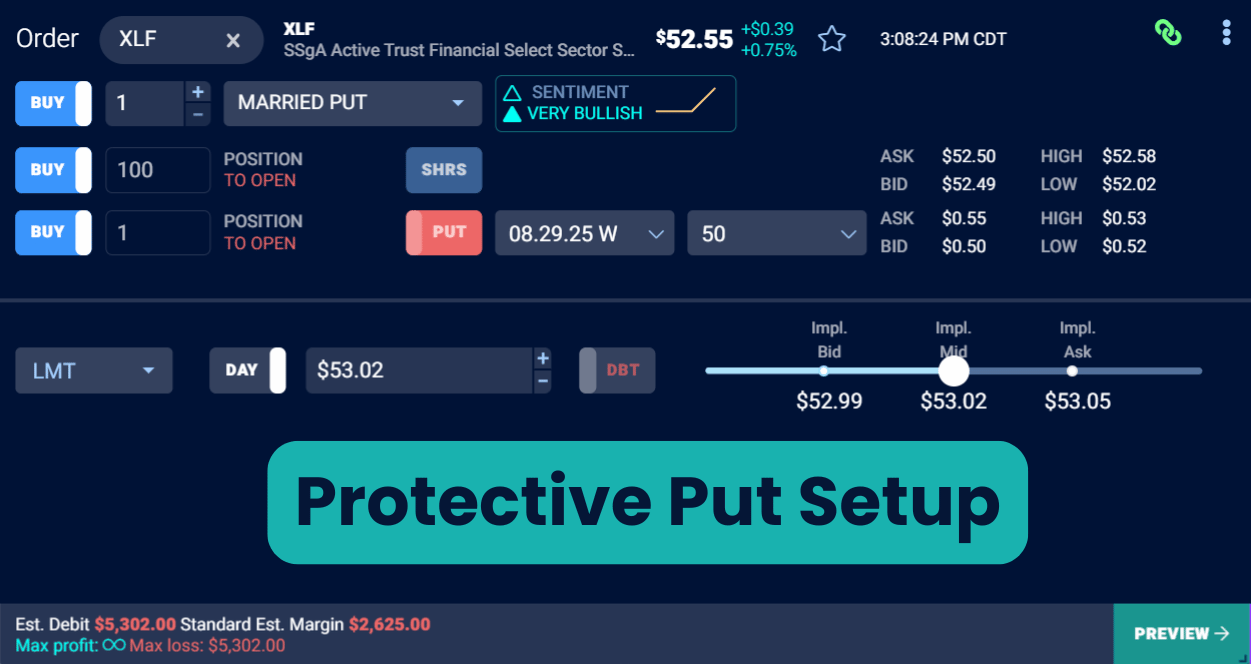

Protective Put: Trade Components

Setting up a protective put (sometimes called a ‘married put’) is relatively easy:

- Purchase 100 shares of stock

- Purchase 1 put option

Generally speaking, the put option is purchased out of the money. If you want to hedge a 5% downturn, your put will be ~5% out of the money.

Most traders use this strategy to hedge a pre-existing stock position, in which case, you’d simply buy the put. You can also initiate the entire trade in one click on the TradingBlock dashboard, as seen below:

Outlook: When To Place a Protective Put

Here are a few scenarios when buying a put option to hedge a stock position may make sense:

- When you want short to medium-term downside protection on a stock you already own

- When you’re up on the position and want to lock in gains without selling

- When you expect volatility ahead (e.g., earnings, Fed meeting, macro events)

- When you’re willing to pay a small premium for peace of mind, while keeping upside potential

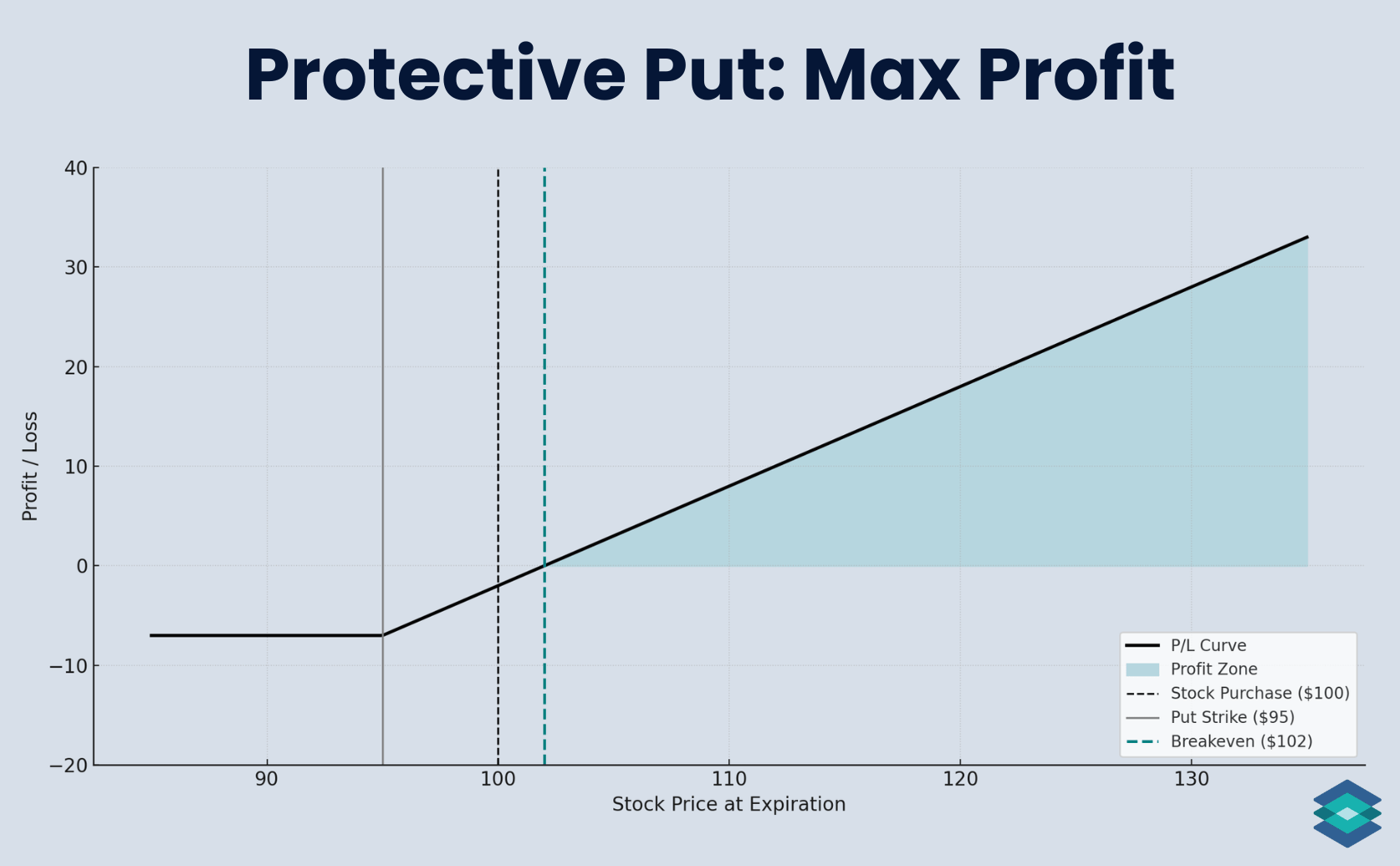

Protective Put Payoff Profile

Let’s now review the maximum profit, loss, and breakeven for this trade.

Protective Put: Max Profit

The maximum profit on a protective put is unlimited, since there’s no cap on how high the stock can go. Just remember: your cost basis is increased by the amount paid for the put.

For example, let’s say you bought ABC stock at $100 per share and a 95 put expiring in one month for $2. Here’s where the maximum profit (unlimited) sits:

If ABC rallies to $135 by expiration:

- The put expires worthless

- You keep the stock gains: $135 – $100 = $35

- Subtract the $2 premium paid → Net profit = $33 per share

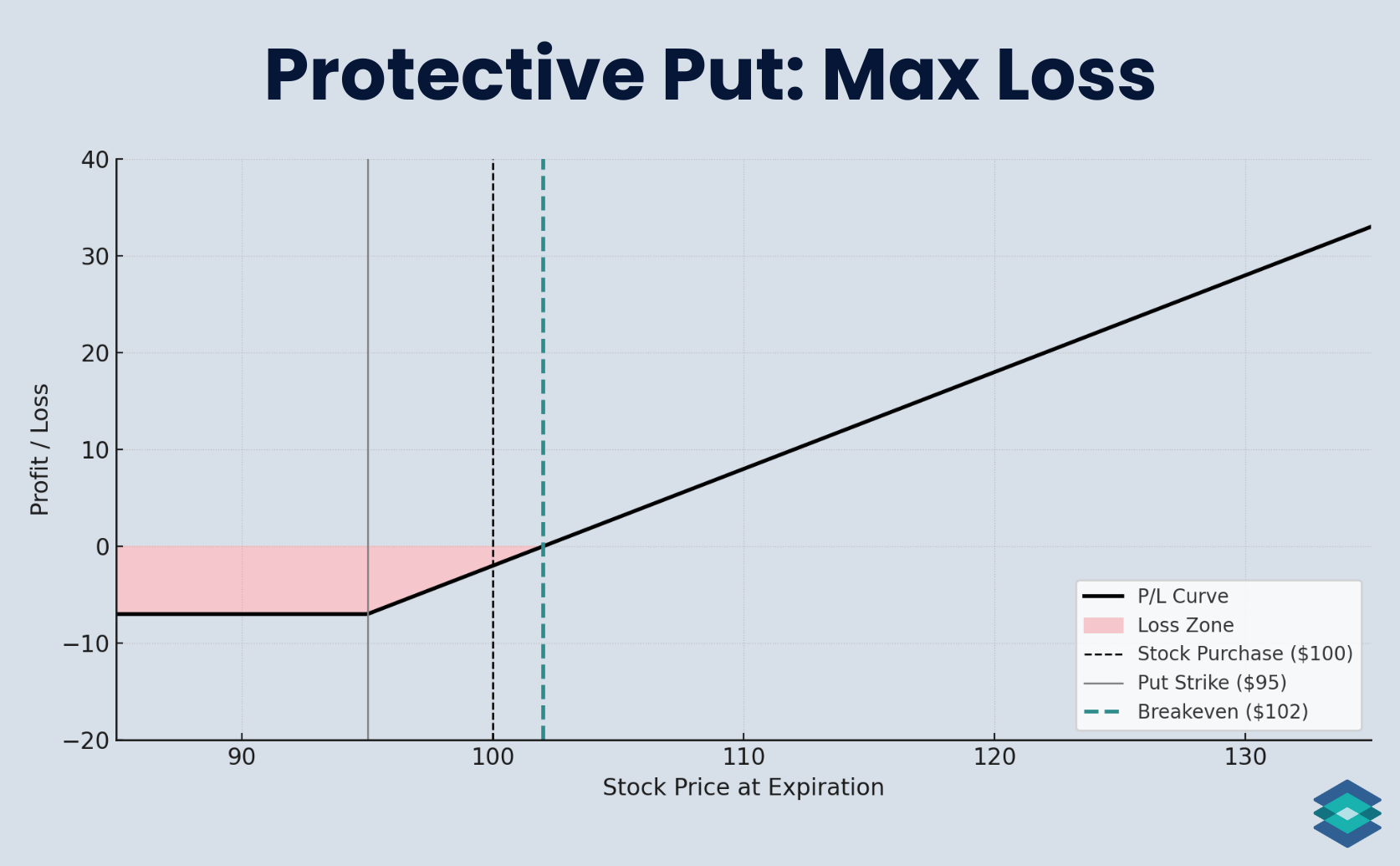

Protective Put: Max Loss

The most you can lose on a protective put trade is the difference between your stock purchase price and the put strike price, plus the premium paid for the put.

- Max loss = (stock price – put strike) + premium paid

Let’s revisit the details of our previous trade:

- Stock purchase price: $100

- Put strike: 95

- Put premium paid: 2

The max loss here would be:

($100 – $95) + $2 = $7 per share,

or $700 total (since each option's contract covers 100 shares). We can see this below:

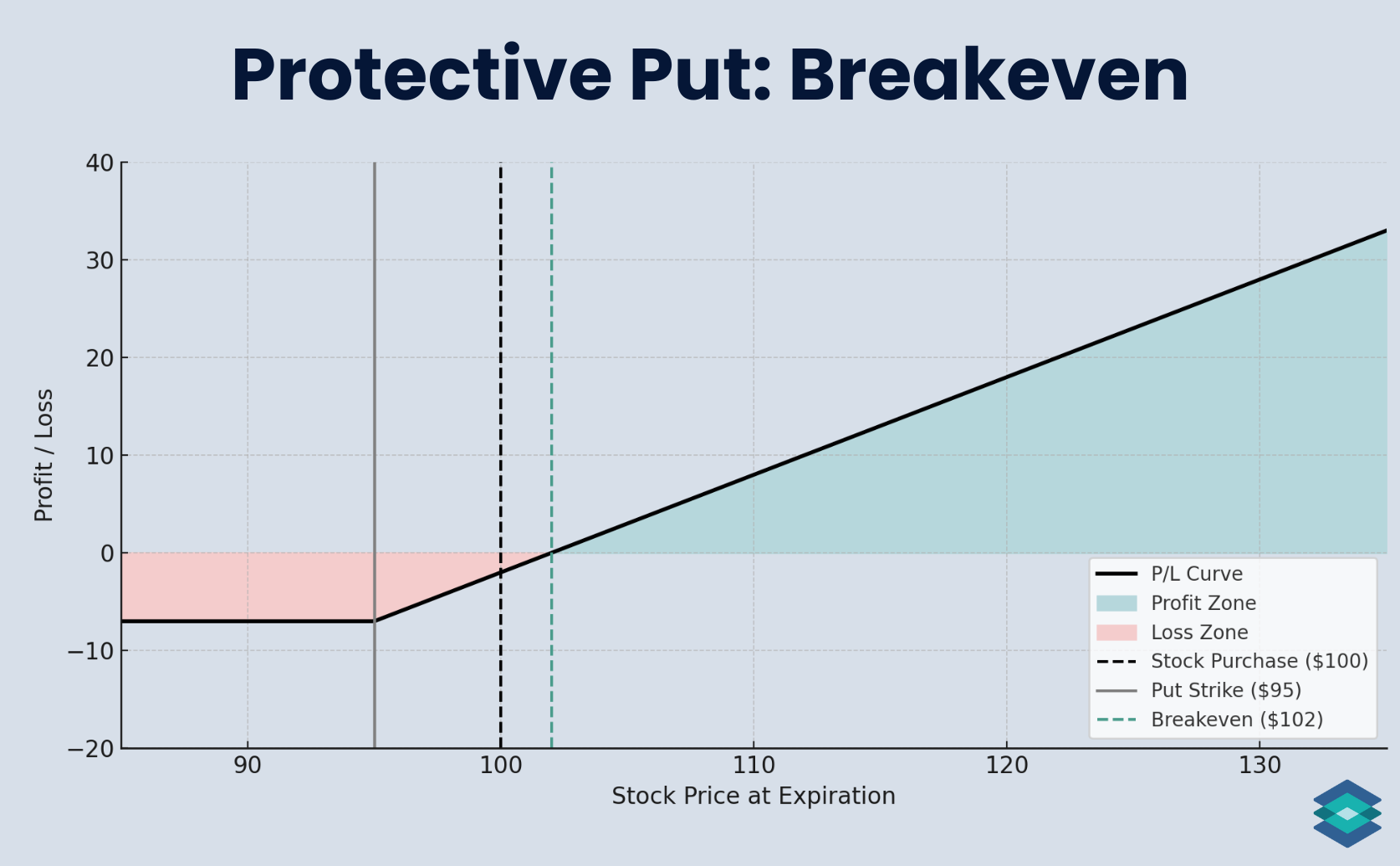

Protective Put: Breakeven

The breakeven on a protective put is straightforward:

- Breakeven = stock price + premium paid

Returning to our previous trade:

- Stock purchase price: $100

- Put strike: 95

- Put premium paid: 2

Our breakeven would therefore be $102 ($100 + $2 put premium) as seen below:

Choosing Your Strike Price

When choosing the strike price of your put option, you're going to have to weigh some trade-offs:

- Lower strike = cheaper, less protection

- Higher strike = more expensive, tighter protection floor

Think of it as buying insurance: the more coverage you want, the more you’ll pay. Most traders select a strike price slightly below the current stock price to protect against moderate price drops without overpaying for the hedge. I prefer buying puts that are about 3–5% out of the money.

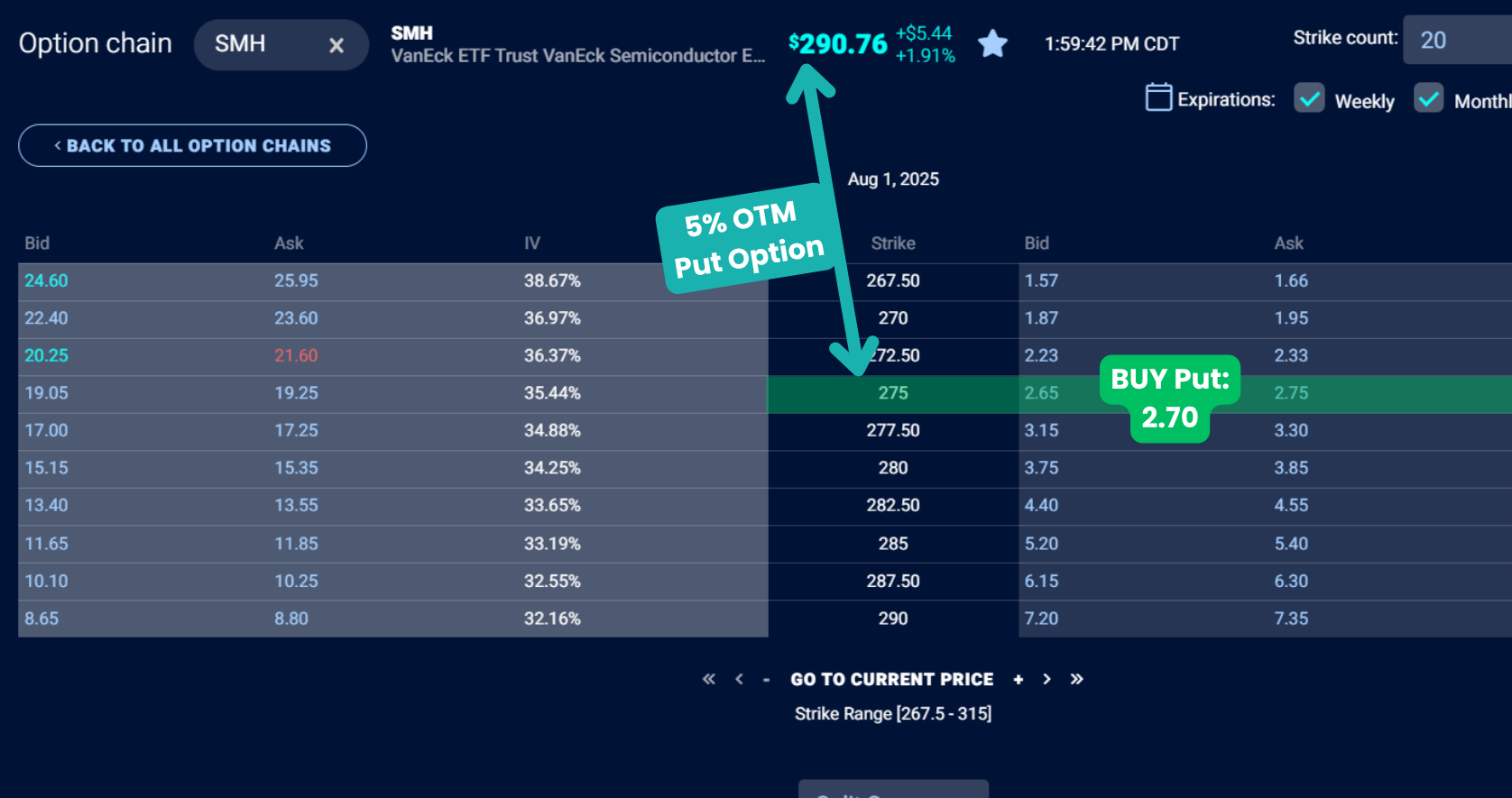

Protective Put Trade Example: SMH

In this example, we will buy a protective put on SMH (VanEck Semiconductor ETF).

We’ll enter the stock and the put option simultaneously for simplicity’s sake. Still, please note that most protective puts are added after the long stock position is purchased, typically to protect a gain.

We want to own the stock, but we also want to hedge against some semiconductor earnings that are expected to be released in about two weeks.

Let’s head over to the TradingBlock dashboard to find a put option about 5% out of the money:

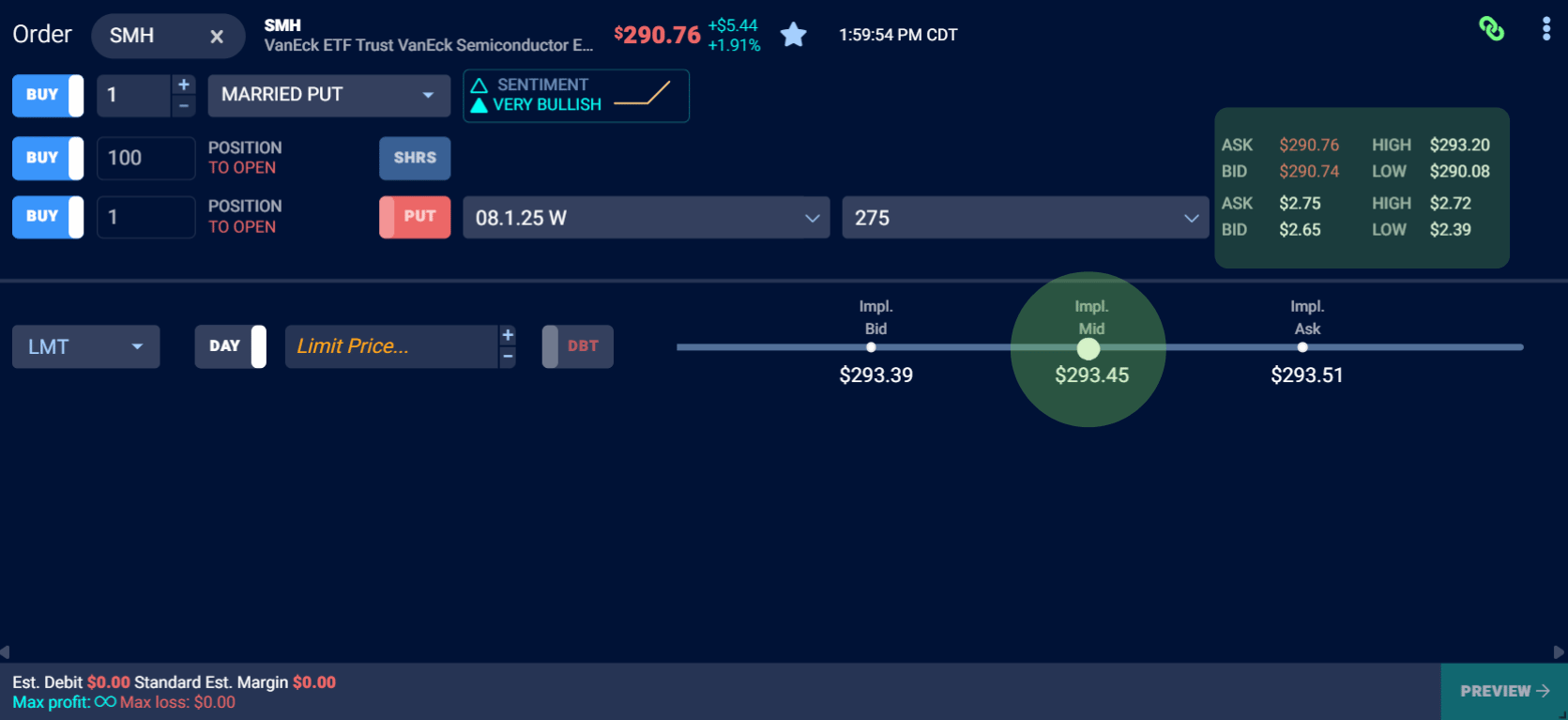

So we’re going to buy 100 shares of SMH and buy 1 put option with a 275 strike price for 2.70.

When trading options, it’s always best to start at the midpoint. If you don’t get filled right away (and want to), work the order up in penny or nickel increments. Read more about options liquidity here!

We're going to assume we got filled at the midpoint on this trade for a total cost of 293.45, as seen below:

SMH Trade Details

And here are the details of the trade we just put on:

- Shares Bought: 100 SMH @ 290.75

- Buy 1 Put: Strike 275 @ 2.70 mid

- Net Debit Paid: 290.75 (stock) + 2.70 (put) = 293.45 total cost

- Breakeven: 293.45

- Max Loss: 293.45 cost – 275 put strike = 18.45 per share ($1,845 total)

- Max Profit: Unlimited (stock can rise forever)

- Profit Zone: Max gain if SMH rallies; protection kicks in below 275

- Risk/Reward: Risking $1,845 to stay long with defined downside

Let’s now explore a few trade outcomes:

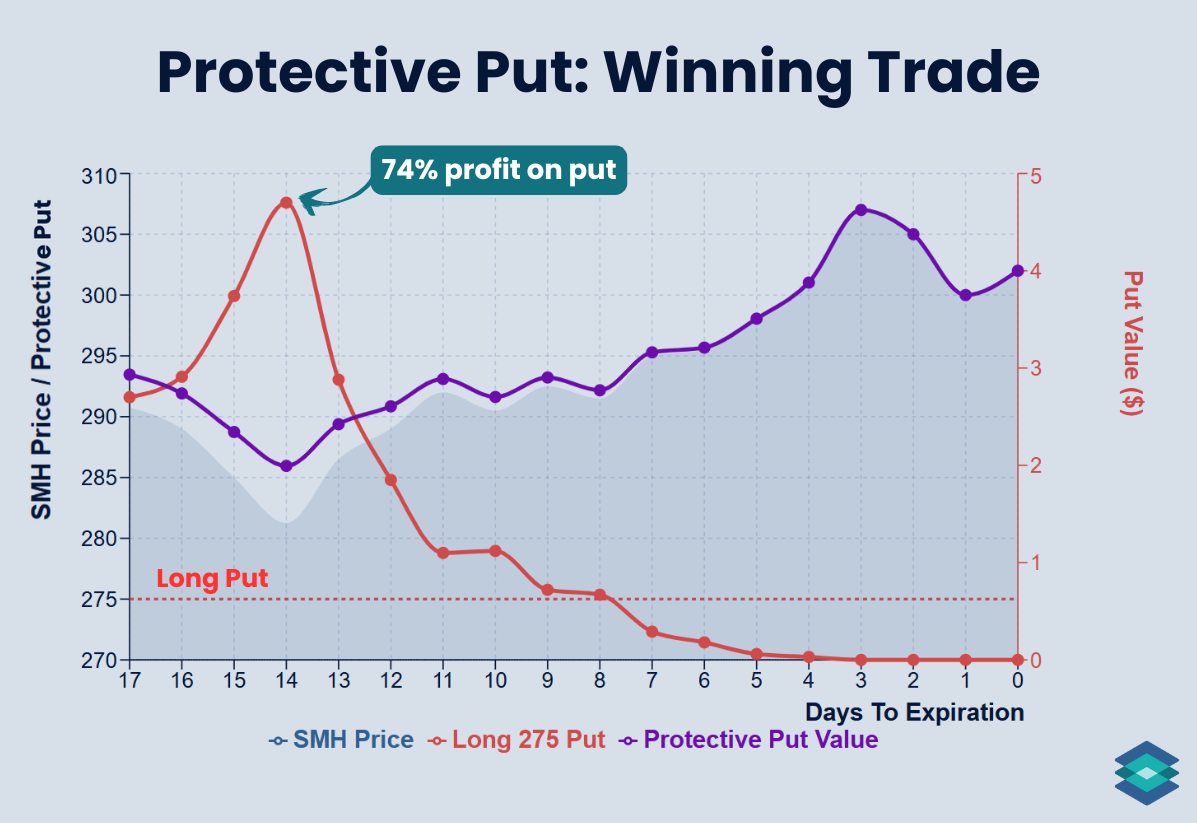

SMH Winning Trade Example

Seventeen days have passed, and option expiration is upon us. SMH rallied as we anticipated, closing at $302/share. The long put expired worthless; we lost the full premium, but we made up for it on the stock side.

Here’s how our trade played out:

- SMH Price: $290.75 → $302 ⬆️

- Expiration: 17 days → 0

- Shares Bought: 100 @ $290.75

- Buy 275 Put: $2.70 → expired worthless

- Net Cost Basis: $293.45 (290.75 stock + 2.70 put)

- Net Gain: $302 – 293.45 = $8.55 per share ($855 total)

- All-In Result: Stock rallied, put wasn’t needed, and gains were locked in above breakeven

Under the Hood: Winning Trade

And here’s how our trade played out in real time:

Early on in the trade, we experienced some volatility. Our put was valued at $4.70 with 14 days to expiration. If you were expecting a reversal here, you could have sold the put for a 74% profit and rolled the trade out unhedged, leaving only the stock position.

SMH Losing Trade Example

In this outcome, semiconductor earnings were dismal, sending the ETF plunging and our put soaring. At expiration, SMH closed at $255, down 12.3% from our entry.

Here’s how things settled:

- SMH Price: $290.75 → $255 ⬇️

- Expiration: 17 days → 0

- Shares Bought: 100 @ $290.75

- Buy 275 Put: $2.70 → $20

- Net Cost Basis: $293.45 (290.75 stock + 2.70 put)

- Net Loss: 293.45 – 275 = $18.45 per share ($1,845 total)

- Percent of Max Loss Realized: 100% of defined risk

- All-In Result: Stock dropped sharply, but losses were capped thanks to the put

Let’s now see how the trade played out in real time:

Under The Hood: Losing Trade

.png)

As we can see above, around the 11 DTE mark, SMH began experiencing significant volatility. The stock tanked, but we were fully hedged with our long 275 put. Without that protection, buying 100 shares at $290.75 and holding through expiration at $255 would have resulted in a loss of $3,075. The protective put dramatically changed that outcome.

Since the put gave us the right to sell at 275, our effective exit value was $275 per share. We paid $2.70 for the put, bringing our total cost basis to $293.45. That means our maximum loss was $293.45 minus $275, or $18.45 per share, which comes out to a total of $1,845.

Once SMH fell below the strike, every additional dollar lost on the stock was offset by a dollar gained on the put. The hedge did exactly what it was designed to do.

Protective Puts and Time Decay

Assuming the underlying asset's price and implied volatility (IV) stay flat, out of the money options steadily lose value over time. That’s because with each passing day of no movement, the underlying asset has less time to reach the strike price.

This is known as time decay, and it accelerates significantly in the final 45 days leading up to expiration, as illustrated below:

.png)

I like to keep my long put in the 30–90 days to expiration (DTE) range. If it drops below a month, I’ll usually roll the put out, typically as part of a calendar spread, to push it back toward 90 days. This way, I stay effectively hedged without letting my long put decay down to pennies. It’s a lot better to roll an option when it’s worth $2 than when it’s down to $0.05.

Choosing Your Deltas

In options trading, delta tells you two things:

- How much an option moves for every $1 move in the stock

- The probability that an option expires in the money

When buying protective puts, a delta around 0.30 strikes the right balance between cost and coverage for me. Go too low, say, below 0.10 delta, and you're barely protected. Go too high, and you’re paying so much premium that you might be better off just trimming the stock instead.

Protective Puts and Implied Volatility

Implied volatility (IV) plays a huge role in how much you’ll pay for a protective put. When IV is high, options become more expensive across the board. That usually means the market is expecting bigger moves, whether from earnings, macro news, or general fear.

Buying protection in a high IV environment means you’re likely paying up. Sometimes it’s worth it, but if volatility drops after you enter the trade, your put can lose value even if the stock moves lower.

.png)

When IV is low, hedging is cheaper. But it also usually means the market isn’t pricing in much risk.

So, how do you know if IV is elevated? By comparing it to its own historical average. Look at IV rank or IV percentile to see how current volatility stacks up against the past year.

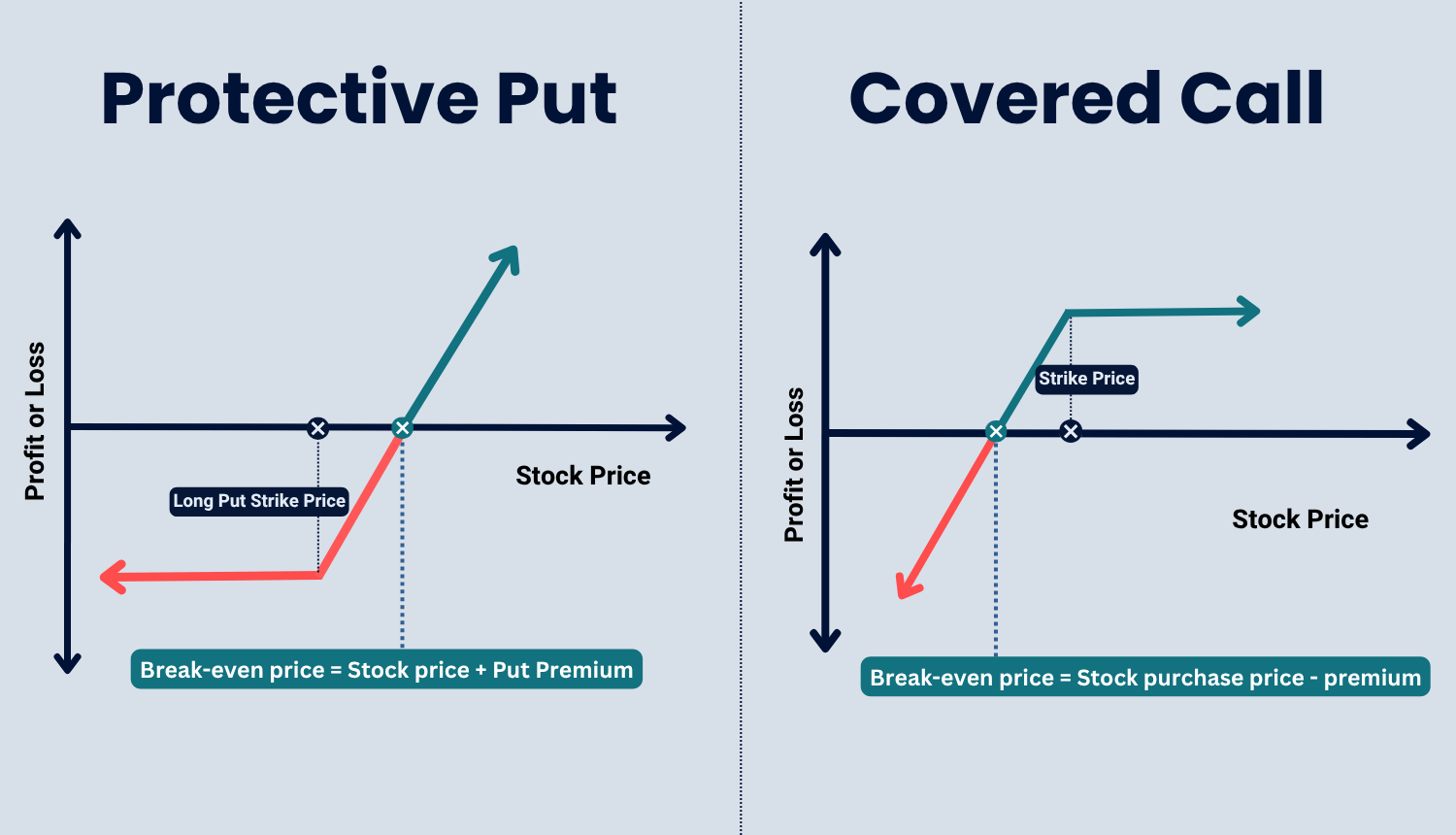

Protective Put vs Covered Call

- Protective Put: Limits downside and keeps upside open, but requires paying a premium

- Covered Call: Generates income and slightly reduces risk, but caps upside potential and offers minimal protection if the stock drops

The protective put and covered call both pair stock with an option, but they serve very different purposes.

A protective put is for downside protection. You’re long stock and long a put, which sets a floor under your position. If the stock price drops, the put option increases in value, thereby limiting losses. This strategy incurs upfront costs, but keeps your upside open. It’s a favorite for short to medium-term hedging without triggering capital gains.

A covered call, on the other hand, is all about income. You’re long stock and short a call, collecting a premium in exchange for capping your upside. If the stock stays flat or rises modestly, the trade works great. But if the stock rallies hard, you get called out. And if it tanks, the call premium barely cushions the loss. It’s a great strategy if you’re neutral to slightly bullish and want to lower your cost basis or earn extra yield.

Managing Protective Puts

Managing a protective put isn’t complicated, but it does take some attention. Here’s how I usually approach it:

- Keep an eye on time. Once the put drops under 30 days to expiration, time decay starts accelerating. I like to roll it out around that point, usually through a calendar spread, to keep protection in place without letting the value bleed out.

- Watch the stock. If the stock rallies and your put is way out of the money, you can either let it expire or roll it up to a higher strike to lock in more gains.

- Plan for auto exercise. If your put is in the money near expiration, ask yourself if you’re ready to sell the stock. If not, roll the put out to a later date or down to a lower strike to stay in the trade without triggering a sale.

Protective Puts and The Greeks

In options trading, the Greeks are a set of risk metrics that help estimate how an option’s price will respond to changes in key market variables. Here are the five most important Greeks to know:

- Delta – shows how much the option price changes for a $1 move in the stock.

- Gamma – shows how much delta shifts when the stock moves $1.

- Theta – shows how much the option loses in value each day from time decay.

- Vega – shows how much the option price changes for a 1% change in implied volatility.

- Rho – shows how much the option price changes for a 1% change in interest rates.

And here is the relationship between protective puts and these Greeks:

⚠️ Protective puts provide downside protection but come at a cost and require a solid understanding of how options work. This strategy may not be suitable for all investors. Premiums, commissions, and slippage can significantly affect trade performance, none of which are reflected in the examples above. Before trading options, read The Characteristics and Risks of Standardized Options.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

FAQ

The protective put is an options trading strategy that involves purchasing an out of the money put option to hedge 100 shares of stock. If the stock falls below the put strike, the position cannot lose more than the difference between the stock price and put strike, plus the premium paid. It’s a simple way to cap downside risk while staying long the stock.

You should buy a long put when you are strongly bearish on the underlying asset, expecting its price to decline significantly.

A protective put is a bullish position. You are long a put option along with 100 shares of stock, so you want the stock to go up, but you’re hedged if it falls.

A protective put involves long stock and a long put. A covered call involves long stock and a short out of the money call. The protective put is more expensive but provides much more downside protection. The covered call limits upside and offers little cushion on the downside.

A protective put is the same trade as a married put. Both involve 100 shares of long stock and one long out of the money put option.

You can roll a protective put if the option is nearing expiration but you still want downside protection, or if the stock has rallied and you want to lock in gains by moving the put strike higher.

A covered call works by buying 100 shares of stock and then selling 1 out-of-the-money (OTM) call option against those shares. Ideally, you enter both legs at the same time as a single trade.

As time passes, the call option ideally falls in value due to time decay (theta). If the stock stays below the strike price by expiration, the call expires worthless—and you keep the full premium.

The biggest downside to a covered call vs. holding stock is that your profit is capped at the premium received plus any stock appreciation up to the strike price, while holding the stock alone allows for unlimited gains.